Navigating the world of Medicare Supplement Plans can be challenging, but understanding your options for 2027 is crucial for optimal healthcare coverage. This guide will walk you through the top-rated plans, offering a comprehensive comparison to help you make an informed decision based on your healthcare needs and budget. Explore the benefits and features of various Medicare Supplement Plans and find the one that aligns with your lifestyle. Whether you’re new to Medicare or re-evaluating your current coverage, this resource provides valuable insights into the Medicare landscape for 2027 and beyond.

Top Rated Medicare Supplement Plans 2027

Key Highlights

- Understand Medicare and Medigap plans to cover gaps and reduce out-of-pocket costs.

- Medigap Plan F offers comprehensive coverage but is limited to existing enrollees post-2020.

- Medigap Plan G provides a balanced option with lower premiums and similar coverage to Plan F.

- Consider personal health needs, location, and financial situation when choosing a plan.

- Utilize MedicarePartCPlans.org for tailored Medigap and Medicare Advantage comparisons.

Compare plans and enroll online

Understanding Medicare Supplement Plans in 2027

As we navigate through the evolving landscape of Medicare in 2027, understanding the intricacies of Medicare Supplement Plans becomes crucial. These plans, also known as Medigap, aim to bridge the coverage gaps inherent in Original Medicare. By exploring an array of options, beneficiaries can enhance their insurance, bringing comprehensive benefits and reducing out-of-pocket expenses. This section delves into the foundational aspects of Medicare and Supplement Plans, and how supplement plans effectively complement Medicare coverage.

Overview of Medicare and Supplement Plans

Coming to grips with Medicare and its Supplement Plans paves the way for making informed decisions regarding healthcare needs. Medicare, the federal health insurance program, primarily serves individuals aged 65 and older, along with certain younger people with disabilities. While it offers a wide array of benefits, Original Medicare, comprised of Part A (hospital insurance) and Part B (medical insurance), may leave beneficiaries with substantial out-of-pocket expenses due to deductibles, copayments, and coinsurance.

This is where Medicare Supplement Plans, known colloquially as Medigap, play a pivotal role. Created to cover gaps in original Medicare coverage, these supplement plans provide financial relief from costs that traditional Medicare doesn’t cover. With private insurance companies offering these plans, the objective is to minimize expenses such as copayments and coinsurance, offering a safety net for unexpected healthcare costs. It’s important to note, however, that these supplement plans don’t replace Original Medicare but work alongside it to enhance insurance coverage.

A crucial aspect of supplement plans is their standardization by the federal government, meaning each plan offers the same benefits, regardless of the insurer. This ensures that whether an individual chooses Medigap Plan F in one state or Plan G in another, the coverage remains consistent. This standardization aids in comparing different Medicare supplement plans effectively and transparently, enhancing beneficiaries’ ability to choose the top-rated options that align with their needs.

Understanding the distinction between Original Medicare and Medicare Supplement Plans is essential for those exploring top-rated options for 2027. Knowing how these plans fit into a broader health insurance strategy can empower beneficiaries to make informed decisions, ensuring comprehensive coverage without unnecessary financial burdens. It’s advised to assess personal healthcare needs, review all potential supplement plan benefits, and consult resources like MedicarePartCPlans.org for customized plan comparisons tailored to specific locales and coverage necessities.

How Supplement Plans Complement Medicare Coverage

Medicare Supplement Plans are designed to work in tandem with Original Medicare, providing a valuable adjunct to the basic coverage already available. These supplement plans, by covering the gaps left by Original Medicare, offer a comprehensive safety net that can substantially limit out-of-pocket expenses. When understanding the specifics of how these plans complement Medicare coverage, one should explore the array of benefits that Medigap plans bring to the table.

Firstly, by alleviating costs such as copayments, coinsurance, and deductibles associated with Medicare Parts A and B, supplement plans relieve financial stress for beneficiaries. This becomes particularly important for those frequently accessing medical services, as the accumulation of these costs can be significant without supplemental insurance. Additionally, certain Medigap plans extend benefits that include coverage for foreign travel emergencies, a boon for retirees who spend time abroad.

The strategic complementarity of Medigap plans ensures that while preserved, beneficiaries have predictable healthcare expenses. With standardized offerings from A through N, beneficiaries can customize their coverage based on specific healthcare needs. Notably, high-deductible versions of some plans are available, which can reduce premium costs while maintaining critical coverage for catastrophic health events.

Moreover, Medigap plans also play a pivotal role in dispelling the financial unpredictability often associated with healthcare. This predictability is achieved by covering the percentages of medical service costs not included in Original Medicare, thus delivering comprehensive coverage. Additionally, some plans cover Part B excess charges, ensuring that beneficiaries aren’t caught off guard by unexpected doctor fees and afford uninterrupted access to their preferred healthcare providers.

In choosing the best Medicare Supplement Plans for 2027, it’s essential to assess individual health needs and budgetary constraints. Comparing these plans with other options, such as Medicare Advantage, can further refine choices, although both pathways offer distinct benefits. By utilizing tools like MedicarePartCPlans.org’s free Medicare plans finder tool, beneficiaries can secure valuable insights tailored to their specific locale and requirements, making the complex landscape of Medicare Supplement Plans less daunting.

Popular Medigap Plans for Comprehensive Coverage

Navigating the complex landscape of Medicare Supplement Plans, or Medigap, requires understanding the most popular options that provide comprehensive coverage. These plans help fill coverage gaps left by Original Medicare, offering a layer of financial security and enhancing existing benefits. This section delves into the benefits and coverage features of top-rated Medigap plans such as Plan F, Plan G, and Plan N, each designed to offer significant supplement benefits and minimize out-of-pocket expenses for beneficiaries.

Exploring the Benefits of Medigap Plan F

Medigap Plan F has long been recognized as one of the most popular Medigap plans for those seeking comprehensive coverage. This plan effectively covers all gaps left by Original Medicare, including Part A and Part B deductibles, copayments, and coinsurance, offering peace of mind to enrollees by ensuring minimal unexpected costs during healthcare visits. The extensive benefits of Medigap Plan F make it a preferred choice, particularly among those who anticipate frequent medical service use.

One of the stand-out features of Medigap Plan F is its coverage for Medicare Part B excess charges, which are the additional fees a healthcare provider may charge above the amount Medicare approves. This feature prevents unpleasant surprises on numerous medical bills, helping to streamline healthcare budgeting for retirees. Additionally, Plan F covers foreign travel emergency services, paying for 80% of approved costs after a deductible, an important factor for those who regularly travel abroad.

Despite its popularity, it should be noted that Plan F was phased out for new enrollees as of January 1, 2020, due to legislative changes aimed at recalibrating cost structures and promoting fiscal responsibility among beneficiaries. However, those who were already enrolled by that date can continue receiving the plan’s comprehensive benefits. This transition means that newly-eligible Medicare beneficiaries may need to explore other options, like Plan G or Plan N, which also provide robust coverage but differ slightly in benefits structure.

For existing beneficiaries or those enrolled before 2020, Plan F remains a powerful tool that mitigates out-of-pocket healthcare expenses. Understanding its comprehensive coverage can reassure individuals that their healthcare needs are financially managed, allowing them to focus on maintaining health and wellness without the stress of potential medical costs. As beneficiaries evaluate their options, considering the enduring benefits of Plan F in comparison with other plans on the market helps in making well-informed healthcare decisions.

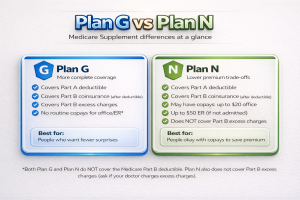

Analyzing the Coverage of Medigap Plan G

Medigap Plan G stands out as a top-rated alternative to Plan F, especially for new beneficiaries seeking comprehensive coverage while navigating the Medicare landscape. Offering nearly identical benefits to Plan F, Plan G covers all Part A deductibles and foreign travel emergency healthcare, safeguarding beneficiaries against the financial uncertainties of unexpected medical needs. The primary distinction lies in Plan G’s exclusion of the Medicare Part B deductible, which shifts a modest financial responsibility to the enrollee.

For beneficiaries pivoting from Plan F, Plan G’s comprehensive coverage can be appealing due to its similarities in benefits and broad scope of coverage. It includes full coinsurance for hospital and outpatient costs, blood transfusion expenses, and hospice care, ensuring significant cost-relief across many healthcare settings. Plan G’s strategic balance between coverage and affordability makes it a favored choice, as it usually comes with lower premium costs than Plan F, making it appealing for budget-conscious individuals who are comfortable managing the annual Part B deductible themselves.

An advantage of enrolling in Plan G is its adaptability to various healthcare needs and its potential long-term cost advantages. Even after accounting for the Part B deductible, Plan G’s lower premiums can result in financial savings relative to Plan F, particularly for those who prefer paying small standardized costs instead of higher monthly premiums. This financial predictability is attractive to beneficiaries aiming for sustainable healthcare costs as they transition into post-retirement life.

Plan G’s rising popularity since Plan F’s closure to new enrollees suggests a notable shift toward cost-effective decision-making by beneficiaries striving for comprehensive healthcare solutions. When researching and comparing Medigap options, using resources like MedicarePartCPlans.org can assist in evaluating whether Plan G aligns with their health needs and financial objectives. Moreover, examining regional differences in premiums and coverage availability remains crucial for informed decision-making, given that insurance companies can price premiums differently across states.

Understanding the Features of Plan N

Medigap Plan N emerges as a compelling choice for those prioritizing comprehensive coverage with a touch of cost-effectiveness. Plan N’s features emphasize affordability, making it a go-to option for beneficiaries seeking substantial Medicare supplement benefits without the burden of high premiums. As healthcare costs continue to unsettle retired individuals, Plan N provides a balanced approach with targeted coverage areas.

A highlight of Plan N’s features is its coverage for Part A deductible and hospital coinsurances, affording peace of mind to beneficiaries opting for extensive hospitalization coverage. Unlike Plans F and G, Plan N introduces cost-sharing for certain services; it covers the full coinsurance for outpatient services, but beneficiaries share some costs through modest copayments for doctor office visits and emergency room use (provided one isn’t admitted). Additionally, it doesn’t cover Part B excess charges, meaning beneficiaries should confirm with providers if they accept Medicare assignments, thus ensuring no surprise charges.

The structured cost-sharing under Plan N can be attractive for those who don’t frequently access healthcare services, making it a cost-efficient alternative while still securing comprehensive inpatient and applicable outpatient coverage. This balance of lower premiums and manageable out-of-pocket costs positions Plan N favorably for healthy beneficiaries with predictably low medical needs while still offering protection for high-cost scenarios like extensive inpatient care.

Plan N’s strategic cost-efficiency, compared to more exhaustive options like Plan F and G, reflects in its premium rates, which are often significantly lower. As premiums can vary by location and insurer, evaluating Plan N with a focus on local providers and cost structures is essential. Using tools like the Medicare plans finder available on MedicarePartCPlans.org can offer insights tailored to specific personal and regional needs, ensuring a thoughtful approach to selecting a Medigap plan that harmonizes with both health and financial goals.

In conclusion, weighing the features of Plan N and comparing it with other Medigap options, while accounting for factors like coverage needs, anticipated healthcare usage, and financial preferences, remains a significant step in optimizing Medicare benefits. The decision demands a comprehensive understanding of each plan’s offerings and a commitment to securing the best-suited coverage for individual circumstances.

Find & Compare Plans Online

Choosing the Best Medicare Supplement Plans for Your Needs

Selecting the best Medicare Supplement Plans in 2027 demands a keen understanding of personal healthcare preferences, financial capabilities, and the intricacies of Medigap coverage. With various plans available, beneficiaries can find options tailored to reduce out-of-pocket expenses and enhance overall satisfaction. Evaluating critical aspects of Medigap insurance can simplify decision-making. Moreover, considering how location affects plan choices provides insight into potential variations in coverage. By using resources like MedicarePartCPlans.org, beneficiaries can effectively compare top-rated insurance companies, ensuring their chosen Medigap policy aligns with their individual preferences and needs.

Factors to Consider When Evaluating Medigap Insurance

When selecting a Medigap policy to enhance your Medicare coverage, multiple factors must be considered to ensure it aligns well with your healthcare needs and financial situation. The first critical aspect is the specific benefits the Medigap plans offer. While each plan is standardized, meaning the benefits are consistent regardless of the provider, the extent of coverage for services like foreign travel emergencies, skilled nursing care, and Part B excess charges varies among plans. This standardization aids beneficiaries in decision-making by allowing them to focus on direct comparisons of premiums and additional fees, fostering transparency in the evaluation process.

Cost is another fundamental factor in your Medigap insurance decision. The premium you pay can vary significantly between companies and regions, even for the same Medigap plan. It’s essential to explore different pricing models, like community-rated, issue-age-rated, or attained-age-rated pricing methods. These determine how your premiums may increase over time and impact your long-term financial planning. Comparing the insurance ratings and satisfaction scores of different companies can provide insights into provider reliability and service quality, helping you choose a well-regarded company with competitive premium rates.

Understanding potential out-of-pocket expenses is crucial in evaluating the true cost of Medigap plans. This includes evaluating plan deductibles as well as any copayment or coinsurance obligations. Some plans, like the high-deductible versions of Plan F or Plan G, offer lower premiums in exchange for higher deductible costs, which might be more suitable for those who anticipate fewer medical visits but want robust catastrophic coverage. Accessing up-to-date information from resources like MedicarePartCPlans.org can clarify these financial responsibilities, aiding in your decision-making.

Your healthcare needs, both current and anticipated, should guide your Medigap insurance choice. If you manage multiple medical conditions or frequently visit healthcare providers, a plan offering comprehensive coverage like Plan G might be attractive. Conversely, if your healthcare needs are minimal, Plan N could provide substantial savings on premiums while still offering core benefits. The pivotal step is aligning your plan with anticipated healthcare usage, ensuring the selected coverage prioritizes your satisfaction and peace of mind.

In summary, choosing the right Medigap policy involves careful consideration of several interconnected factors: benefits, costs, provider reputation, and personal healthcare requirements. Utilizing tools like MedicarePartCPlans.org helps navigate these choices, allowing you to systematically compare provider options and select a complementary Medigap plan. With informed decision-making, you enhance your Medicare coverage comprehensively, minimizing out-of-pocket costs and maximizing peace of mind.

How Location Impacts Medicare Supplement Plan Options

Understanding how location affects your Medicare Supplement Plan options is essential for beneficiaries seeking optimized coverage. The geographic region you reside in can profoundly influence the availability and cost of Medigap policies. Each state has a distinct regulatory environment, which means that Medicare supplement plans can vary in pricing and availability. Analyzing the specific offerings in your location provides a vantage point from which to gauge how Medigap insurance might align with your needs and financial constraints.

Firstly, consider that Medigap plans are available nationwide from private insurance companies, but state regulations can affect what options are offered. States like Massachusetts, Minnesota, and Wisconsin have unique standardization models differing from the rest of the country. This means the plans available and the benefits they provide could differ from what’s available elsewhere, potentially impacting your decision if you reside in these states. Therefore, understanding local regulations is crucial to comprehending available plan structures and benefits entirely.

The cost of Medigap plans is another element heavily influenced by location. Factors such as the cost of living, healthcare costs, and regional demographics all play a role in determining premiums. For instance, densely populated urban areas with higher medical costs might see increased premiums compared to rural areas, where expenses may be lower. It’s important to seek quotations from multiple companies within your region to understand the breadth of options available and identify which plans strike a desired balance between comprehensive coverage and cost.

Location can also affect the selection of companies available to you. While many insurers operate nationally, smaller local companies may offer competitive rates that address region-specific needs more effectively. Exploring both national and regional providers can enhance your opportunity to find the best-fit plan for your circumstances. The MedicarePartCPlans.org website is an invaluable resource, as it provides localized plan comparison tools that can assist beneficiaries in identifying and evaluating these location-specific variations efficiently.

Additionally, your healthcare provider options might influence your plan choice. For those residing in areas with limited healthcare providers accepting Medicare assignments, it’s crucial to ensure that your chosen Medigap policy supports the provider networks available to you. This aspect ensures you receive uninterrupted and affordable care, reducing potential inconveniences related to accessing desired medical services.

In conclusion, assessing how your location impacts Medicare Supplement Plan options is paramount to optimizing your insurance strategy. This evaluation enables you to navigate premiums and plan availability, ensuring robust, personalized coverage that accommodates local healthcare conditions. Engaging with resources like MedicarePartCPlans.org can simplify this process, offering tailored insights for informed decision-making, ultimately leading to a satisfactory and financially sustainable Medigap plan selection.

Comparing Medicare Advantage and Medigap Plans

When evaluating comprehensive Medicare coverage, understanding the distinctions between Medicare Advantage and Medigap Plans is crucial. These two plan types offer unique benefits, coverage levels, and cost structures that can significantly impact your healthcare experience. In this section, we’ll explore the key differences between Medicare Advantage and Medigap plans, as well as factors to consider when determining which option might be the most suitable for your specific needs. This comparison will help you navigate the complexities and make an informed choice for 2027.

Key Differences Between Medicare Advantage and Medigap Plans

To appreciate the nuanced decision between Medicare Advantage and Medigap plans, it’s essential to understand their fundamental differences. Medicare Advantage, sometimes known as Medicare Part C, offers an alternative to Original Medicare by bundling coverage normally offered under Parts A and B, and often Part D, into one plan provided by private companies. These plans are customizable based on provider networks, such as Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs), delivering a more comprehensive approach to coverage through managed care. They may include additional benefits like vision, dental, and wellness programs, appealing to those looking for all-inclusive healthcare plans with predictable out-of-pocket expenses. However, Medicare Advantage plans may have network restrictions, requiring beneficiaries to seek care from specific doctors and hospitals.

In contrast, Medigap plans serve as a complement to Original Medicare by covering out-of-pocket expenses such as copayments, coinsurance, and deductibles, which Medicare Part A and B do not cover. These plans, also known as Medicare Supplement Insurance, are standardized by the federal government, making the benefits consistent across providers. However, this standardization enables easier comparison of options like Plan F, G, and N, which offer varied coverage levels suitable for different needs and budgets. While Medigap does not provide coverage for prescription drugs or additional benefits like vision or dental, it allows for a broader choice of healthcare providers since it’s not restricted by network agreements.

A critical decision factor involves the cost structure: Medigap plans typically involve higher monthly premiums than Medicare Advantage plans, but can lead to lower overall expenses for frequent medical treatments as they reduce out-of-pocket costs. Meanwhile, Medicare Advantage plans are cost-effective for those who infrequently seek medical care, offering low or zero premiums with comprehensive benefits. It’s vital to weigh these factors along with individual healthcare needs, lifestyle, and risk tolerance when selecting a suitable plan. Resources like MedicarePartCPlans.org offer tools to help beneficiaries understand their coverage options, focusing on location-specific plans to optimize decision-making.

| Plan Characteristics | Network & Coverage | Cost Structure | Additional Benefits |

|---|---|---|---|

| Medicare Advantage | Utilizes a network of providers; may require referrals and have geographical restrictions. | Lower monthly premiums; costs can vary depending on services used. | May include additional benefits like vision, dental, and wellness programs. |

| Medigap | No network restrictions; coverage across various providers nationwide. | Typically higher premiums; more predictable out-of-pocket costs. | Does not generally offer extra benefits; it focuses on covering out-of-pocket expenses from Original Medicare. |

This table captures the primary contrasts between Medicare Advantage and Medigap plans, showcasing their differences in structure, coverage, and financial implications for potential beneficiaries.

Factors to Weigh When Comparing Medigap Plans to Medicare Advantage

As you delve into the decision between Medicare Advantage and Medigap plans, several factors warrant careful consideration to ensure an optimal fit for your health coverage needs. One of the foremost aspects is healthcare usage patterns; individuals with complex medical needs or those who frequently travel might favor Medigap for its flexibility, as it covers any provider accepting Medicare nationwide without the limitation of networks. Conversely, Medicare Advantage plans may suit those seeking more integrated health services within a set geographic area, especially when supplemented through additional benefits such as fitness programs or dental care.

Financial considerations are also paramount. Medigap premiums can be higher but benefit those preferring financial predictability by minimizing out-of-pocket expenses. The choice among top-rated Medigap plans such as Plan F, G, or N involves evaluating potential costs such as deductibles alongside anticipated healthcare utilization. Medicare Advantage plans, however, may offer lower premiums and include drug coverage, which can be economical for beneficiaries not frequently accessing services. Reviewing the comprehensive coverage and potential caps on out-of-pocket costs provided by Medicare Advantage plans is essential, along with how these affect your budget and financial peace of mind.

Moreover, satisfaction levels connected to both plan types should be reviewed by evaluating past policyholder experiences and ratings. Companies offering either type of plan can vary greatly in service quality, reliability, and client support. It’s wise to consider the provider’s reputation through reviews and satisfaction ratings, as they can significantly influence the customer experience. For those opting for the freedom of traditional Medicare bolstered by Medigap’s outsized coverage protection, satisfaction often correlates to predictable access to preferred healthcare outlets and minimal billing surprises.

Personalized considerations play a crucial role, such as regional availability of certain plans or provider networks influencing accessibility to covered care providers. Furthermore, exploring how initiatives like MedicarePartCPlans.org’s plans finder tool can aid in comprehensively comparing Medicare Advantage and Medigap options tailored to your location remains a vital step. Such tools streamline the placement process by pinpointing plans that match closely with individual financial constraints and health care priorities, ultimately facilitating a choice aligned with personal, comprehensive coverage goals. By weighing these considerations thoughtfully, beneficiaries can achieve both enhanced coverage and satisfaction from these top-rated Medicare plan options in 2027.

Utilizing MedicarePartCPlans.org's Medicare Plans Finder Tool

Maximizing the benefits of Medicare supplement plans in 2027 requires a resourceful tool that simplifies plan comparisons. MedicarePartCPlans.org provides a free Medicare plans finder tool designed to help beneficiaries navigate their options seamlessly. By utilizing this tool, you can explore a wide range of top-rated Medicare plans tailored to your specific healthcare needs and budgetary constraints. The tool aids in comparing premiums, benefits, and coverage details, making it easier to select a plan that aligns with your requirements.

How to Compare UnitedHealthcare Plans Effectively

When diving into the world of UnitedHealthcare options and comparing Medicare plans effectively, several strategies come into play. UnitedHealthcare, recognized for its extensive offerings in Medicare Advantage and Medicare supplement plans, demands a nuanced approach to ensure beneficiaries find the optimal coverage matching their unique healthcare needs. Understanding UnitedHealthcare’s AARP-branded Medicare resources, beneficiaries can harness insights tailored for enhanced satisfaction and a comprehensive coverage experience. First, explore UnitedHealthcare’s diverse Medicare plans by focusing on the primary factors influencing plan effectiveness, coverage, costs, benefits, and satisfaction. Using tools like MedicarePartCPlans.org’s finder tool can simplify this extensive process, allowing beneficiaries to sort through the myriad options available.

Beneficiaries should start by understanding the different plans under UnitedHealthcare, a leading provider in the Medicare insurance space, to find suitable Medicare plans. UnitedHealthcare offers plans ranging from Medicare Advantage, Medicare Part C, frequently bundling additional benefits like dental, vision, and wellness programs, to Medigap or supplement plans. Each option provides varying degrees of support depending on the beneficiary’s needs. Medicare Advantage is ideal for those who value additional benefits and are comfortable with network-based healthcare services. In contrast, Medigap offers broader provider access, ideal for those preferring freedom in choosing healthcare providers without network constraints.

As you compare UnitedHealthcare Medicare plans, evaluating the costs, deductibles, premiums, copayments, and potential out-of-pocket expenses is integral. Utilize the MedicarePartCPlans.org tool to compare variable costs like premiums and deductibles, focusing on understanding how these affect your financial health in retirement. For Medicare supplements, consider standardized plans like Plan F, G, or N, gauging each against personal financial and healthcare dynamics, keeping in mind that premium variations may be noticeable due to factors such as age, smoking status, and geographic location.

The benefits and comprehensive coverage offered by UnitedHealthcare’s Medicare plans are pivotal to the decision-making process. Some plans integrate extras such as routine vision and dental care, gym memberships, and prescription drug coverage, valuable for those with chronic conditions requiring consistent medication. For supplement plans, understanding coverage gaps in original Medicare and how these are bridged can reduce unexpected costs. Additionally, consider provider satisfaction ratings, as companies with high customer satisfaction scores often deliver better overall service, reinforcing the importance of selecting a trusted provider.

For beneficiaries evaluating UnitedHealthcare’s options, leveraging comprehensive tools and educational resources on platforms like MedicarePartCPlans.org becomes imperative. Such resources provide a structured approach to reviewing plan specifics, enhancing provider satisfaction clarity, balancing premium costs, coverage breadth, and anticipated health service utilization. By systematically comparing factors and utilizing helpful resources, individuals are better equipped to make informed decisions, aligning personal Medicare coverage needs with financial realities. Ultimately, the journey to finding the right UnitedHealthcare plan becomes less daunting, enabling strategic planning for health and financial peace of mind in retirement.

As you navigate the nuances of comparing UnitedHealthcare Medicare plans, consider these essential tips to streamline your decision-making process:

- Identify key health needs and prioritize coverage features that address them effectively.

- Analyze plan details, including premiums, copayments, and out-of-pocket maximums.

- Review provider networks to ensure preferred doctors and specialists are included.

- Consider additional benefits like vision, dental, or wellness programs that add value.

- Compare customer satisfaction ratings to gauge service quality and plan reliability.

- Use online tools for a comprehensive comparison of available plans.

- Balance coverage options against anticipated healthcare utilization in retirement.

These steps will support a well-informed decision, aligning coverage choice with personal needs and financial goals.

Finding the right Medicare Supplement plan can be a crucial step in ensuring comprehensive healthcare coverage. As you evaluate your options, consider factors such as out-of-pocket costs, coverage benefits, and your current healthcare needs. Consulting with a knowledgeable source or leveraging user-friendly tools can greatly assist in making an informed decision. Whether you are new to Medicare or reviewing your current plans, staying informed about changes and updates in plan offerings will help ensure that your healthcare needs are effectively met. For further assistance, exploring our comparison resources can offer valuable insights tailored to your specific situation.

Compare plans and enroll online

Frequently Asked Questions

What are Medigap plans and how do they complement Original Medicare?

Medigap plans, also known as Medicare Supplement Plans, are designed to cover out-of-pocket costs not included in Original Medicare, like deductibles, copayments, and coinsurance. They help minimize expenses for beneficiaries by providing financial relief from costs that traditional Medicare doesn’t cover.

How do Medigap Plan F, Plan G, and Plan N differ from one another?

Medigap Plan F offers comprehensive coverage but is closed to new enrollees post-2020. Plan G provides almost similar benefits to Plan F minus the Part B deductible, often at a lower premium. Plan N covers Part A deductible and most coinsurances but includes copayments for some doctor and emergency visits, offering a cost-effective option for many.

How are Medicare Advantage plans different from Medigap plans?

Medicare Advantage (Part C) combines Original Medicare Parts A and B and often Part D, providing additional benefits like vision and dental. These plans operate within a network of providers. In contrast, Medigap supplements are used alongside Original Medicare to cover additional costs without network restrictions. They do not include extra benefits such as prescription drugs.

What factors should be considered when choosing a Medigap plan?

Consider your healthcare needs, budget, and location when selecting a Medigap plan. Understand standard benefits, compare premium costs, and assess out-of-pocket expenses. Utilize comparison tools, like those found on MedicarePartCPlans.org, to make an informed decision based on your circumstances.

How does location impact Medicare Supplement Plan options?

Geographic location can affect the availability and cost of Medigap plans due to regional regulations and variations in healthcare costs. Comparing plans within your specific region is crucial to ensure an appropriate fit for your needs and budget, as outlined by resources like MedicarePartCPlans.org.

Have Questions?

Speak with a licensed insurance agent

1-877-436-2343

TTY users 711

Mon-Fri: 8am-9pm ET

Find & Compare Plans Online

ZRN Health & Financial Services, LLC, a Texas limited liability company