Exploring Medicare Advantage plans can be a complex journey, especially when uncovering potential hidden costs associated with Part C. Our in-depth guide aims to clarify these costs, helping you make informed decisions regarding your healthcare coverage. Whether you’re new to Medicare or reviewing your current enrollment, understanding the nuances of Medicare Advantage plans is crucial. This page details common hidden expenses and shares practical insights to empower you in selecting an option that aligns with your healthcare needs and budget. Dive in to navigate the landscape of Medicare Part C with confidence.

Hidden Costs in Medicare Part C Plans

Key Highlights

- Medicare Advantage (Part C) plans provide alternatives to Original Medicare with added benefits.

- Hidden costs in these plans can include copayments, coinsurance, and deductibles, impacting annual expenses.

- Coverage gaps often occur without supplemental insurance, affecting areas like dental and vision care.

- Online tools aid in comparing Medicare Advantage plans by location, ensuring tailored coverage.

- Utilize resources like MedicarePartCPlans.org to understand plan variations and manage healthcare effectively.

Compare plans and enroll online

Understanding Medicare Advantage (Part C) Plans

Medicare Advantage plans, also known as Part C, present an alternative way for eligible recipients to receive their Medicare benefits. Unlike Original Medicare, these plans are offered by private insurance companies approved by Medicare. They cover all the services that Original Medicare offers, and often include additional benefits and services. This section sheds light on how Medicare Advantage is distinct from Original Medicare and explains the eligibility and enrollment periods necessary for these plans. Understanding these differences is crucial for planning and choosing the right coverage to meet your healthcare needs and budget.

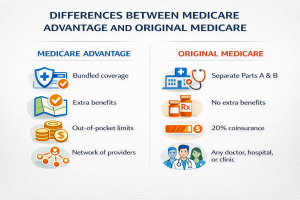

What Makes Medicare Advantage Different from Original Medicare?

Medicare Advantage plans stand out due to their unique structure compared to Original Medicare. One of the primary differences lies in the coverage offered. While Original Medicare, comprising Part A for hospital services and Part B for medical coverage, provides a standardized level of healthcare services, Medicare Advantage plans often include additional benefits like vision, dental, and hearing, catering to broader healthcare needs.

These plans also frequently cover prescription drugs, an option only available separately under Part D with Original Medicare. This consolidated approach makes them appealing, especially for those looking for more comprehensive healthcare solutions within a single plan.

Another critical difference is the involvement of private insurance companies in administering Medicare Advantage plans. These companies have the latitude to structure plans with varying features like network restrictions, such as Health Maintenance Organization (HMO) or Preferred Provider Organization (PPO) plans. Choosing the right network can impact your out-of-pocket costs and the services you receive. Each plan typically has a maximum out-of-pocket limit, offering a safety net that Original Medicare does not provide, which can alleviate concerns about unexpected medical expenses.

Though these plans offer several benefits, they come with certain limitations. One must understand that each Medicare Advantage plan has its own network of doctors and hospitals, which could limit the healthcare providers you have access to. Additionally, while supplemental benefits are available, they may be associated with additional premiums. It’s vital to weigh these factors and assess how a Medicare Advantage plan might meet your healthcare needs effectively compared to Original Medicare. By doing so, you can make informed decisions about your insurance plan, considering both the upfront coverage and any backend costs that might arise.

Eligibility and Enrollment Periods for Medicare Advantage

Navigating the eligibility and enrollment periods for Medicare Advantage plans is crucial for ensuring timely coverage. Typically, eligibility begins when you turn 65, though those under 65 with certain disabilities or conditions, such as End-Stage Renal Disease, may also qualify. It’s essential to confirm your eligibility beforehand, as this will guide your ability to enroll and receive comprehensive coverage under these plans.

The enrollment process for Medicare Advantage occurs mainly during the Initial Enrollment Period (IEP), which starts three months before you turn 65, includes the month of your birthday, and extends three months afterward. This period provides a seven-month window to join a Medicare Advantage plan, allowing new enrollees to select plans that best fit their healthcare preferences and budget. If you’re already enrolled in Original Medicare, you can switch to a Medicare Advantage plan during this time.

Special Enrollment Periods (SEPs) offer a chance to make changes outside the standard windows due to specific life events. Events like moving out of your plan’s service area, losing other health coverage, or being eligible for both Medicare and Medicaid are typical circumstances allowing for adjustments in Advantage plan enrollment. Understanding these periods will help you plan your healthcare coverage more strategically, avoiding coverage gaps and undue financial burdens.

Additionally, the Annual Election Period, or Open Enrollment Period for Medicare Advantage, occurs from October 15 to December 7 each year. During this time, beneficiaries can reevaluate their healthcare needs and switch plans if necessary. It’s a beneficial opportunity to adjust current plans to better suit changing health conditions or lifestyle needs. Learning about these periods and eligibility criteria is key to maximizing the benefits that Medicare Advantage plans offer.

If you’re considering switching plans or enrolling, it’s wise to utilize available resources, such as the free Medicare plans finder tool on MedicarePartCPlans.org, to compare options effectively based on your location and coverage requirements.

Following these enrollment guidelines can simplify your Medicare Advantage planning. Here are key considerations to help with your decision-making process:

- Check your eligibility criteria if you’re under 65 with a qualifying condition.

- Note the seven-month Initial Enrollment Period timeline around your 65th birthday.

- Use the Annual Election Period to reassess and adjust plans as needed.

- Be aware of Special Enrollment Periods for changing life circumstances.

- Compare different Medicare Advantage plans using available online tools.

- Regularly evaluate your healthcare needs to ensure chosen plans align with current health and budget.

These strategies will aid in navigating Medicare Advantage effectively and avoiding any potential pitfalls.

Hidden Costs in Medicare Advantage Plans

Understanding the hidden costs associated with Medicare Advantage plans is essential for managing your healthcare budget effectively. While these plans can offer comprehensive coverage, they often come with additional costs that are not immediately apparent. Consider out-of-pocket expenses such as copayments, coinsurance, and deductibles, which can significantly impact your annual healthcare expenses.

In this section, we’ll explore some of these common hidden costs, explain how Medicare Advantage plans balance costs and coverage, and offer strategies to anticipate and manage these expenses, ultimately helping you make well-informed decisions regarding your health coverage.

| Cost Aspect | Description | Potential Impact | Mitigation Strategies | Considerations |

|---|---|---|---|---|

| Premiums | Monthly payments required to maintain coverage. | Can vary annually, sometimes increasing unexpectedly. | Compare plans regularly; seek guidance from a financial advisor. | Evaluate premium stability over past years. |

| Out-of-Pocket Expenses | Costs paid directly by beneficiaries aside from premiums. | Includes copayments, deductibles, and coinsurance which can accumulate. | Choose plans with a cap on out-of-pocket expenses. | Consider the maximum out-of-pocket limit when choosing a plan. |

| Network Restrictions | Providers or facilities must be within the plan’s network. | Receiving care outside the network may result in higher costs. | Verify network adequacy and flexibility. | Check if preferred providers are included. |

| Additional Benefits | Includes services like dental or vision not covered by traditional Medicare. | May involve additional costs or reduced benefits elsewhere. | Balance the utility of extra benefits against overall costs. | Assess the necessity of additional services carefully. |

This table succinctly encapsulates the diverse and complex elements of hidden costs in Medicare Advantage Plans. By outlining key areas such as premiums, out-of-pocket expenses, network restrictions, and additional benefits, it assists beneficiaries in understanding and managing their costs effectively by highlighting the potential impact and offering strategic considerations for informed decision-making.

Identifying Common Out-of-Pocket Expenses

When delving into Medicare Advantage plans, it’s crucial to identify common out-of-pocket expenses that could affect your overall costs. Although these plans aim to provide comprehensive coverage, they often include expenditures such as copayments, coinsurance, and deductibles that aren’t immediately clear. Copayments typically involve fixed fees that apply when you visit healthcare professionals or receive medical services.

These baseline fees might seem minor, but they can add up considerably, especially if you require frequent medical attention or specialist visits. Coinsurance is another aspect where you’ll share a percentage of the medical costs, which can vary significantly based on the services and your specific plan’s guidelines.

One often overlooked area is prescription drug coverage, which, although frequently included in Medicare Advantage plans, might come with varying costs. The deductible for drug coverage is an upfront cost before your insurance kicks in, and it’s key to pay attention to these details within your plan’s specifics. Some medications might not be covered fully, leading to additional out-of-pocket expenses. Moreover, the out-of-pocket maximum is the cap on what you’ll spend annually from your pocket, but understanding how it applies across different services, including those involving hospital stays or outpatient services, can provide invaluable insights into your financial planning.

Apart from these direct costs, supplemental costs can arise from services not entirely covered under your plan. Dental, vision, and hearing may often need extra coverage, requiring you to plan effectively to offset these expenses. It’s vital to evaluate these potential costs to ensure your chosen Medicare Advantage plan aligns with your healthcare needs while keeping budget considerations in check. By identifying these possible supplemental costs and other unexpected expenses within Medicare Advantage, beneficiaries can better prepare for their healthcare financial obligations.

Find & Compare Plans Online

How Advantage Plans Balance Costs and Coverage

Medicare Advantage plans strive to balance costs and coverage by blending comprehensive healthcare services with financial constraints. One way they manage this balance is by offering additional coverage that Original Medicare doesn’t provide, such as vision, hearing, and dental services. However, these extras often come with added insurance costs, which are among the hidden costs that beneficiaries need to be aware of. Advantage plans commonly involve network restrictions like HMOs or PPOs, which can affect your choice of healthcare providers and, consequently, your out-of-pocket expenses.

Each Advantage plan contains a built-in out-of-pocket maximum, serving as a cost-containment feature to protect beneficiaries from excessive medical expenses annually. While this is a significant advantage over Original Medicare, it’s crucial to understand how network services impact these costs. In-network services might be entirely or partially covered, but out-of-network services could incur higher costs or no coverage at all. This highlights the importance of checking the network details and considering potential added costs when planning your healthcare budget.

Additionally, the back-end costs of Advantage plans include elements like premium payments alongside Original Medicare premiums. Evaluating these alongside potential out-of-pocket expenses can offer a clearer lens into the total cost of the coverage. Understanding how costs are structured within Advantage plans helps beneficiaries anticipate financial responsibilities and better manage healthcare expenditure.

By leveraging the benefits of supplemental and routine services, paired with a solid plan for managing potential unexpected costs, you can make informed choices about your Medicare Advantage coverage. Effective planning will ensure that your chosen plan meets both your healthcare needs and financial capabilities.

Coverage Gaps in Medicare Advantage Plans

Medicare Advantage plans offer a host of benefits, but it’s essential to be aware of potential coverage gaps that might affect your healthcare journey. Understanding these gaps can help you anticipate hidden costs and formulate strategies to manage them effectively. We’ll delve into how certain services may not be covered and the implications this can have on your medical expenses. Additionally, we’ll explore practical strategies to manage these unexpected costs and discuss how supplemental coverage can play a critical role in bridging these gaps, ensuring you make well-informed decisions about your health insurance.

Exploring Potential Coverage Gaps and Their Implications

Medicare Advantage plans, while beneficial, can include various potential gaps in coverage that might lead to unforeseen medical costs. Coverage gaps occur when certain healthcare services or needs are not fully covered by the plan, leaving beneficiaries responsible for additional out-of-pocket expenses. These gaps can significantly impact medical costs, especially for those who require frequent or specialized healthcare services.

For instance, while many Advantage plans offer extensive hospital and medical service coverage, they may limit coverage for areas such as dental, vision, or hearing care. These services often require supplemental coverage, which can mean extra costs for beneficiaries.

The implications of these potential coverage gaps extend beyond just the services themselves. They can affect your overall financial health, as hidden costs like copayments and higher deductibles emerge when accessing certain types of care. Insurance companies often set strict network restrictions, and using providers outside this network could lead to higher medical expenses or even denial of coverage.

As these plans have coverage limits, understanding them is crucial for comprehensive healthcare planning. A thorough gap analysis can reveal these potential gaps and guide you in selecting appropriate supplemental coverage options to mitigate unexpected costs.

Furthermore, the complexity of Medicare Advantage plans means that beneficiaries must pay attention to plan limitations, especially when it comes to treatment plans and specialist visits. The lack of clear understanding can lead to unintended back-end costs, making healthcare planning vital. By being aware of coverage gaps and their implications, beneficiaries can take proactive steps in selecting the right plan structure or considering additional insurance support to ensure all possible health needs are met. This strategic approach helps avoid potential financial burdens, enabling long-term healthcare stability.

Strategies to Manage Unexpected Expenses

Effectively managing unexpected expenses is crucial when dealing with the various coverage gaps that can arise in Medicare Advantage plans. One primary strategy is thorough planning and awareness of these potential gaps in the services your selected plan offers. Delving into the specifics of your plan regarding network coverage, deductible amounts, and out-of-pocket maximums can provide a clear understanding of the maximum costs you might face.

Integrating supplemental insurance can also be a proactive measure. Supplemental coverage, such as Medigap, helps cover out-of-pocket costs that Medicare Part C might not fully pay, such as copayments or deductibles for hospital stays and other healthcare services. This additional coverage can be particularly beneficial for those who anticipate needing regular medical services not covered by their Medicare Advantage plans, thus cushioning the impact of unexpected medical expenses.

Another essential aspect of managing expenses is keeping track of healthcare services and aligning them with plan benefits. Taking the initiative to conduct periodic expense reviews and cost assessments can identify where extra costs are occurring. This allows you to adjust your healthcare strategy accordingly, whether it’s by choosing in-network providers to reduce expenses or exploring other Medicare Advantage options during the Annual Election Period.

Lastly, leveraging the free Medicare plans finder tool available at MedicarePartCPlans.org can be a helpful resource in comparing coverage gaps and plan costs across different locations. This tool assists in finding the best fit for your needs while minimizing hidden costs and maximizing coverage within your financial constraints. By employing these strategies, beneficiaries can more effectively manage the surprising expenses tied to Medicare Advantage plans, thus safeguarding their health and financial well-being.

Compare Medicare Advantage Plans by Location

Understanding the intricacies of Medicare Advantage plans, especially on a regional level, is crucial for maximizing your healthcare benefits. These plans vary widely by location, and using online tools can significantly enhance your ability to find the most suitable options. With varying network coverage, costs, and supplemental benefits, having a strategy for comparing Medicare Advantage plans can greatly aid in planning your healthcare needs and managing your budget effectively.

Using Online Tools to Find the Best Plan for Your Needs

In today’s digital age, utilizing online tools for planning and comparing Medicare Advantage plans is an invaluable resource for beneficiaries. These tools offer a location-based comparison of various plans, allowing you to assess regional advantage plans effectively. When you start comparing Medicare Advantage plans, it’s essential to consider the network and coverage each plan offers. Different insurance companies provide varying levels of services, making the plan comparison an insightful step toward smarter healthcare decisions.

Online comparison tools allow you to input your location and instantly see which plans are available in your region. This is key because Medicare Advantage plans and network coverage can differ significantly based on where you live. By leveraging these tools, you can identify plans with the best network, helping ensure that your preferred healthcare providers are covered. Additionally, understanding deductible structures and potential coverage gaps becomes more manageable, aiding in better planning and cost management.

Most online tools also enable cost comparisons, highlighting both premium costs and out-of-pocket maximums. This feature helps you understand potential expenses and supports in making informed decisions about supplemental insurance or Medigap policies if needed. Moreover, these tools provide a snapshot of benefits that extend beyond usual medical services, such as dental or vision coverage, which can be crucial for comprehensive healthcare planning.

Another advantage of these tools is that they support planning for future health needs by allowing a detailed review of plan benefits and costs. As your personal healthcare requirements evolve, these resources can guide you in adjusting your coverage efficiently. Regularly using these tools keeps you informed about any changes in Medicare-approved healthcare services in your area, ensuring your insurance plan remains aligned with your health needs and budget constraints.

To enhance your search, consider using the free Medicare plans finder tool available at MedicarePartCPlans.org. This resource can be particularly beneficial for location-based services and uncovering the most fitting Medicare Advantage plans that meet your unique needs. Through this tool, navigating the complex array of plans becomes more straightforward, empowering you to optimize your insurance coverage effectively. With these strategic online resources, beneficiaries can more easily manage healthcare choices, minimizing hidden expenses while maximizing benefits.

Exploring the hidden costs in Medicare Part C plans can help beneficiaries make informed decisions about their healthcare coverage. Although Medicare Advantage plans offer valuable options for those seeking comprehensive care, it is essential to understand potential out-of-pocket expenses. Careful examination of co-pays, network restrictions, and annual out-of-pocket limits will provide clarity and prevent unexpected costs.

Utilize online resources, like MedicarePartCPlans.org, to compare plans by location and evaluate benefits against personal health needs. With proper research, Medicare beneficiaries can select an option that aligns with their financial and medical preferences.

Compare plans and enroll online

Compare Medicare Advantage Plans by Location

What are Medicare Advantage plans?

Medicare Advantage plans, also known as Part C, offer an alternative to Original Medicare by providing additional benefits. These plans are administered by private insurance companies approved by Medicare and typically include services Original Medicare does not, such as vision, dental, and prescription drug coverage.

What are the hidden costs associated with Medicare Advantage plans?

Hidden costs in Medicare Advantage plans may include copayments, coinsurance, and deductibles. These expenses can accumulate throughout the year, impacting your annual healthcare budget. It’s essential to review these costs in each plan carefully to avoid surprises.

How do Medicare Advantage plans differ from Original Medicare?

The main difference between Medicare Advantage and Original Medicare is in coverage. While Original Medicare primarily covers hospital and medical services, Medicare Advantage plans often include additional benefits such as vision, dental, and hearing services. They may also incorporate prescription drug coverage, unlike Original Medicare which requires a separate Part D plan for such drugs.

What are the enrollment periods for Medicare Advantage plans?

Enrollment for Medicare Advantage plans typically occurs during the Initial Enrollment Period, which begins three months before turning 65. There’s also an Annual Election Period from October 15 to December 7 each year. Special Enrollment Periods may be available due to certain life events, allowing changes to your plan outside these standard periods.

How can I compare Medicare Advantage plans effectively?

Comparing Medicare Advantage plans can be made easier using online tools that factor in your location. At MedicarePartCPlans.org, you can compare plans based on network coverage, costs, and benefits to ensure they meet your healthcare needs and budget considerations.

Have Questions?

Speak with a licensed insurance agent

1-877-436-2343

TTY users 711

Mon-Fri: 8am-9pm ET

Find & Compare Plans Online

ZRN Health & Financial Services, LLC, a Texas limited liability company