With the ever-evolving landscape of healthcare, understanding the annual changes to Medicare Supplement Plans for Parts A and B is crucial for making informed decisions. In 2027, beneficiaries must be aware of crucial updates affecting costs, coverage, and plan availability. This guide explores the essential adjustments in Medicare Supplements, delving into factors influencing premiums, specific benefits, and alterations that impact plan selection. Stay informed to optimize your Medicare benefits effectively, comparing available options to ensure they meet your healthcare needs and financial expectations. Explore the changes and discover how they may affect your Medicare journey.

Annual Changes to Medicare Supplement Plans

Key Highlights

- Medicare Supplements 2027 brings important changes affecting costs, coverage, and plan availability.

- Annual adjustments to Parts A & B impact premiums, deductibles, and supplementary benefits.

- Open Enrollment is crucial for reassessing Medicare plans and responding to changes effectively.

- Original Medicare differs from Advantage Plans in provider access, benefits, and cost structures.

- 2027 plan updates include deductible and premium adjustments, altering supplement plan choices.

Compare plans and enroll online

Understanding Annual Changes to Medicare Supplement Plans in 2027

Navigating the world of Medicare can sometimes feel overwhelming, especially with the annual changes to Medicare Supplement Plans. As we approach 2027, it’s important for beneficiaries to understand how these updates might impact their coverage, particularly with Medicare Parts A and B. By having a clear grasp of the accepted coverage changes, beneficiaries can make informed decisions. We’ll also look at how the Medicare Open Enrollment period plays a crucial role in these modifications. Staying informed ensures that retirees and their caregivers are better equipped to adapt to new policy shifts in the upcoming years.

How Changes Affect Parts A & B

The annual adjustments to Medicare Supplement Plans, particularly for Parts A and B, can significantly influence how beneficiaries manage their health insurance needs. Recognizing the nuances of these changes is crucial for anyone relying on Medicare for health coverage. In 2027, expected adjustments might include alterations in deductible amounts and premium rates, which are typically reviewed yearly to align with inflation and healthcare cost trends. These changes can impact how Medicare insurance plans work with Original Medicare to cover healthcare services, potentially affecting out-of-pocket expenses for enrollees.

Medicare Part A and Part B are foundational to Original Medicare, covering hospital and medical services, respectively. Changes to these parts may influence how supplementary plans fill the gaps, such as covering the costs not paid by Original Medicare. For instance, if there’s an increase in the Part A deductible or Part B premium, a supplementary plan might adjust its benefits or premium to compensate. Consequently, beneficiaries may see shifts in their monthly premiums or changes in their plan’s benefits.

Engaging with these plans also requires a keen understanding of Medicare coverage limits and the benefits provided by supplement plans. Beneficiaries should stay informed about insurance plan adjustments since shifts in Medicare rules can alter coverage satisfaction levels or the need for additional coverage. Moreover, understanding these changes before they go into effect can help beneficiaries make decisions about whether to keep their existing plan or explore new options that might fit their healthcare needs better. Utilizing resources like MedicarePartCPlans.org can aid in comparing these options effectively.

The Role of Medicare Open Enrollment

The Medicare Open Enrollment period is a pivotal time for beneficiaries to reassess their Medicare coverage choices in light of yearly changes. This period, occurring annually from October 15 to December 7, provides an opportunity for enrollees to make informed adjustments to their plans. Throughout these weeks, beneficiaries can switch Medicare Advantage and Part D plans or return to Original Medicare if they desire a change in their insurance coverage.

Understanding the open enrollment process can enable beneficiaries to respond to accepted coverage changes effectively. During this period, they can evaluate how parts of their existing Medicare plan perform and decide if the adjustments for the following year serve their needs better. This proactive approach is particularly important for those whose current supplement plan terms might no longer align with their healthcare requirements or financial capabilities.

Furthermore, accessing detailed information about Medicare changes beforehand ensures beneficiaries make well-informed decisions. The changes may also include new plan offerings or discontinuations, which makes it essential to explore the available options comprehensively. Beneficiaries are encouraged to utilize online tools and resources such as MedicarePartCPlans.org to research different insurance plan options and compare benefits, costs, and coverage specifics conveniently.

Insurance plans during Medicare open enrollment require careful consideration to address the unique needs of beneficiaries. It’s crucial to understand the implications of changes and how they affect their personal healthcare strategy and financial planning. By leveraging all available resources and acting during this pivotal period, Medicare beneficiaries can optimize their insurance coverage to align with their healthcare needs and budget.

Impacts on Original Medicare and Medicare Advantage Plans

With annual changes to Medicare Supplement Plans on the horizon, it’s essential to understand how these adjustments impact both Original Medicare and Medicare Advantage Plans. As beneficiaries prepare for 2027, being aware of the differences between these insurance plans and evaluating their options during open enrollment can lead to better coverage decisions. This section delves into the differences between Original Medicare and Medicare Advantage Plans, and guides beneficiaries on how to assess their plan options effectively.

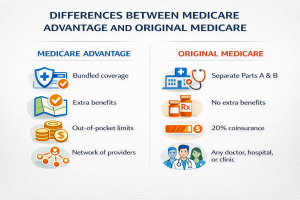

Differences Between Original Medicare and Advantage Plans

Original Medicare consists of Part A, covering hospital services, and Part B, focusing on outpatient care, both of which are governed directly by the federal government. Meanwhile, Medicare Advantage Plans, also known as Part C, are offered by private insurance companies that contract with Medicare to provide Parts A and B benefits. One of the primary differences is that while Original Medicare provides broad access to numerous healthcare providers nationwide, Medicare Advantage Plans often have network restrictions, which can limit available provider options based on the plan’s specific network criteria.

Enrollees choosing Original Medicare often supplement their coverage with Medigap policies to help cover out-of-pocket costs like deductibles and coinsurance not otherwise covered. In contrast, Medicare Advantage Plans may offer additional benefits, such as vision, dental, or wellness programs, which are not included in Original Medicare. These extra benefits can be appealing; however, their inclusion often comes at the cost of flexibility. Beneficiaries should evaluate whether the plans’ networks and benefits align with their healthcare preferences and geographic needs.

Furthermore, the cost structure between these plans differs. While Original Medicare generally requires separate premiums for Parts A, B, and sometimes Medigap, Medicare Advantage enrollees typically pay a single premium that may even include Part D (prescription drug coverage). It’s vital to review how these cost differences align with personal budget considerations. The benefits offered by Medicare Advantage Plans can be attractive to those who prefer consolidated insurance coverage or engage in less frequent travel that might necessitate broader provider access.

Deciding between Original Medicare and Medicare Advantage Plans requires a thorough evaluation of one’s healthcare needs, lifestyle, and financial situation. Beneficiaries should consider using resources like MedicarePartCPlans.org to compare various insurance plans and understand potential out-of-pocket expenses. Understanding these differences is crucial to making an informed decision about which plan best meets an individual’s healthcare strategy and personal preferences.

When deciding between Original Medicare and Medicare Advantage Plans, it’s essential to weigh several key considerations to ensure the best choice for your needs.

- Consider the flexibility of choosing healthcare providers that Original Medicare offers compared to network restrictions in Medicare Advantage Plans.

- Evaluate if lower out-of-pocket costs in Medicare Advantage align with your financial capabilities and healthcare needs.

- Check if extra benefits like vision or dental in Medicare Advantage are important for your well-being.

- Assess your comfort with potential required referrals for specialists under Medicare Advantage Plans.

- Review whether prescription drug coverage is included or requires a separate Part D plan.

- Think about your preferred ease of managing claims and the potential paperwork involved in each option.

- Investigate the stability and reputation of Medicare Advantage providers in your area.

- Determine how service areas for Medicare Advantage Plans affect your lifestyle and travel preferences.

In the journey of selecting the right plan, understanding these elements empowers you to make an informed choice that suits your unique healthcare needs.

Evaluating Your Medicare Plan Options

Evaluating Medicare plan options is a crucial step for beneficiaries, especially during the Medicare Open Enrollment period. This annual opportunity allows enrollees to review and potentially alter their Medicare Advantage Plans or switch back to Original Medicare based on changes in their healthcare needs and budget. When beginning this evaluation, it’s important to thoroughly assess how current plans meet your expectations and consider the benefits they offer against any premium or network adjustments expected in the upcoming year.

One practical step in evaluating insurance plans is to compare the specific benefits they provide, especially for those newly eligible for Medicare or those reconsidering their current choice. Evaluating if additional coverage, such as vision or dental, is necessary, and if so, whether it’s adequately covered by a privately managed Medicare Advantage Plan, is crucial. Additionally, consider how prescription costs are managed through available Part D options in each plan, as these might affect both out-of-pocket costs and medication accessibility.

It’s also essential to factor in the flexibility and choice of healthcare providers available through Original Medicare versus Medicare Advantage Plans. Those valuing the freedom to select any provider may prefer sticking with Original Medicare. However, if cost and convenience of additional services take precedence, Medicare Advantage may present a more streamlined option. As beneficiaries explore, understanding the plan’s details, such as network coverage, co-pays, and potential out-of-network fees, is necessary for an accurate comparison.

Medicare benefits change annually, and keeping abreast of these changes through resources like MedicarePartCPlans.org can provide valuable insights into making informed decisions. With tools available to compare options by location and coverage needs, beneficiaries are better able to strategize their insurance plan choices in alignment with personal healthcare strategies and evolving health needs. The right evaluation process not only aligns with current needs but anticipates future healthcare transitions, ensuring that Medicare enrollees remain covered in a way that is both comprehensive and cost-effective.

| Feature | Original Medicare | Medicare Advantage Plans | Considerations |

|---|---|---|---|

| Provider Choice | Wide availability of providers; not limited to a network | Limited to the plan’s network of providers | Consider network limitations and out-of-network coverage needs |

| Additional Benefits | Primarily covers hospital and medical services | Often includes additional benefits such as vision, dental, or wellness | Evaluate the necessity of extra benefits for personal health needs |

| Cost Structure | Costs can vary, with separate premiums for Part A and Part B | May have lower monthly premiums, but include copayments and other costs | Assess total out-of-pocket expenses in contrast to Original Medicare premiums |

| Out-of-Pocket Cap | No cap on out-of-pocket expenses | Includes an annual out-of-pocket spending limit | Important for those concerned about high healthcare spending |

| Prescription Coverage | Not included; requires a separate Part D plan | Often included in plans | Consider whether bundled prescription coverage is beneficial |

This table highlights the contrasts and considerations between Original Medicare and Medicare Advantage Plans, assisting beneficiaries in making informed decisions.

Find & Compare Plans Online

Lower Prices and Cost Adjustments

Understanding the annual changes to Medicare Supplement Plans is crucial for beneficiaries looking to navigate the 2027 landscape with greater financial assurance. These updates often involve adjustments in monthly premiums and benefits, influencing the cost management strategies for enrollees. By examining the anticipated decrease in prices and the requisite cost adjustments, Medicare beneficiaries can better prepare for how these changes might influence their coverage options under Parts A and B. Knowing what to expect in terms of pricing can empower you to make informed decisions during Medicare open enrollment periods.

How Annual Changes Influence Costs

Annual changes to Medicare Supplement Plans can significantly impact the financial landscape for beneficiaries, primarily through cost adjustments that inform monthly premium variations and out-of-pocket expenses. Each year, adjustments are made to align with the current trends in healthcare costs and inflation rates. For beneficiaries, these changes can translate to modifications in their monthly budget allocations dedicated to healthcare. It is crucial to keep abreast of such fluctuations, as price increases can affect the affordability of certain plans, prompting a reassessment of your current coverage needs.

The adjustment amounts set annually can influence both the rise and fall of premiums. While some changes may increase financial obligations, others might offer the benefit of lower prices, allowing beneficiaries to redirect savings to other essential expenditures. An increase in plan costs often requires beneficiaries to re-evaluate their current supplement plan choices, especially if there are shifts in benefits, or consider other plans that offer greater value for their specific healthcare needs. Understanding the nuances of these changes ensures that you, as a beneficiary, can effectively manage costs while maximizing the coverage provided by Medicare Part A and B supplements.

Furthermore, these annual change dynamics aren’t isolated solely to cost increases. They also include beneficial adjustments such as better benefits packages without increased costs. Staying informed about these changes can facilitate smarter decision-making, especially during the open enrollment period. By leveraging online tools and extensive informational resources, including MedicarePartCPlans.org, beneficiaries can navigate the complexities of selecting the appropriate insurance plan that caters to both their medical and financial requirements, ensuring comprehensive coverage without unnecessary expenses. Being proactive allows you to take full advantage of any advantageous changes in your Medicare coverage, adapting quickly to any necessary modifications.

Strategies to Manage Medicare Costs

Managing Medicare costs effectively is a fundamental component for beneficiaries aiming to maintain financial stability as they plan for healthcare expenses under changing Medicare supplement landscapes. The strategies employed can be diverse, ranging from comprehensive plan analysis to utilizing supplemental resources for better cost management. When faced with annual changes and pricing adjustments, having a strategy in place allows beneficiaries to maneuver these shifts with confidence and assurance.

One of the most effective strategies is to conduct a thorough review of your current Medicare supplement plan. Assess whether the benefits offered align with your existing and anticipated healthcare needs, particularly in light of cost increases or benefit alterations. This assessment should include a detailed comparison of other available plans and their associated costs, ensuring that your choice delivers maximum benefits at a manageable premium. MedicarePartCPlans.org provides a valuable online resource for comparing Medicare plans, enabling you to identify plans that offer cost-effective coverage tailored to your personal health and financial situation.

Furthermore, advocating for preventive healthcare services can aid in managing costs effectively. Medicare Parts A and B offer a variety of preventive services that can reduce out-of-pocket expenses over time by catching potential health issues early before they require more costly interventions. By prioritizing these services, beneficiaries can anticipate lower medical costs, potentially offsetting premium increases and other monthly expenses.

Finally, crafting a personalized financial plan that anticipates possible future changes in both income and healthcare requirements is essential. Beneficiaries should consider potential scenarios that could affect their healthcare spending, such as rising medical needs or a change in income, and adjust their plan accordingly. Keeping abreast of annual Medicare updates ensures that your strategy remains relevant and responsive to changes, allowing you to adapt seamlessly to new Medicare policies and cost structures. These proactive efforts can lead to substantial financial benefits, avoiding unforeseen expenses and securing comprehensive, cost-effective healthcare coverage throughout the year.

2027 Updates on Medicare Plan Benefits

The 2027 updates to Medicare plans bring significant changes that will affect how beneficiaries optimize their supplement plan choices. With evolving benefits and coverage changes, it’s essential to understand how these developments impact both Medicare Parts A and B. Whether you’re currently analyzing your Medicare Supplement options or preparing for changes that go into effect, staying informed is key. This section breaks down what these updates mean for your Medicare insurance and supplement plan choices and offers insights into making informed decisions during the open enrollment period.

What Changes Mean for Supplement Plan Choices

The 2027 updates introduce several noteworthy changes that will influence supplement plan choices, offering Medicare beneficiaries new considerations. These changes are part of a broader effort to align Medicare plans with the current healthcare environment, considering factors like inflation and healthcare cost trends. It’s crucial for beneficiaries to grasp what these changes mean for their existing insurance coverage and future plan selections. For example, if the 2027 updates bring an increase in the Medicare Part A deductible, beneficiaries might see adjustments in their supplement plan premiums to compensate for this change.

Additionally, changes in Part B might alter your decision-making process. Should premium rates increase, it may require evaluating whether your current plan still meets your healthcare and financial needs. It’s essential to consider how these changes will take effect and impact insurance plan benefits. This understanding can lead beneficiaries to rethink their options or even motivate seeking plans that offer better coverage for their specific needs.

Importantly, the flexibility and customization of Medicare supplement plans allow beneficiaries to tailor their coverage based on personal health requirements and geographic location. Access to comprehensive information about these changes, such as through resources like MedicarePartCPlans.org, is invaluable. This site helps you compare plans side-by-side, providing information about coverage and costs to ensure that your choices are well-informed and aligned with upcoming changes.

Understanding these 2027 updates equips Medicare beneficiaries to approach the open enrollment period with confidence. Effectively navigating this period is crucial, as it gives you the opportunity to adjust your supplement plan or explore new options to maintain or enhance your health coverage. By leveraging available resources, staying updated on changes, and assessing your healthcare preferences, you can make strategic insurance choices that align with your health and financial goals.

Staying informed about the anticipated adjustments to Medicare Supplement Plans for Parts A and B in 2027 is crucial for making well-informed healthcare decisions. By understanding these changes, you can ensure that your coverage aligns with your evolving healthcare needs. Evaluate plan options carefully, considering your personal health requirements and budget. For more guidance, explore our free Medicare plans finder tool on our website to compare available plans in your area. This proactive approach will help you navigate changes effectively as you plan for the years ahead.

Compare plans and enroll online

Frequently Asked Questions

What changes can Medicare beneficiaries expect in 2027 regarding Medicare Supplements?

In 2027, Medicare beneficiaries might experience changes in costs, coverage, and availability of Medicare Supplement Plans. These adjustments can impact premiums, deductibles, and supplementary benefits, necessitating careful consideration during plan selection.

Why is the Medicare Open Enrollment period important?

The Medicare Open Enrollment period, occurring from October 15 to December 7 annually, is crucial because it allows beneficiaries to reassess and make changes to their Medicare Advantage and Part D plans or switch back to Original Medicare. This period is essential to adapt to changes in healthcare needs and plan structures for the coming year.

How do the 2027 updates to Medicare plans affect beneficiaries' plan choices?

The 2027 updates introduce potential changes in deductibles and premiums, requiring beneficiaries to evaluate their existing plans. Understanding these changes is crucial for optimizing plan choices to meet healthcare requirements and budget constraints effectively.

What is the difference between Original Medicare and Medicare Advantage Plans?

Original Medicare comprises Part A and Part B, covering hospital and medical services, and allows broad access to providers. Medicare Advantage Plans, or Part C, are privately managed, offering Parts A and B benefits, often with additional services like vision and dental.

How can beneficiaries benefit from resources like MedicarePartCPlans.org?

Resources like MedicarePartCPlans.org enable beneficiaries to compare Medicare plans effectively. These tools offer detailed information on coverage options, costs, and benefits, aiding informed decision-making during open enrollment and plan selection processes.

Have Questions?

Speak with a licensed insurance agent

1-877-436-2343

TTY users 711

Mon-Fri: 8am-9pm ET

Find & Compare Plans Online

ZRN Health & Financial Services, LLC, a Texas limited liability company