Understanding your rights and options under Medicare can be crucial when considering Medicare Advantage, also known as Part C plans. This article sheds light on the concept of issue rights, empowering you to make informed decisions regarding your healthcare coverage. Navigating the complexities of Medicare Advantage plans can often raise questions, especially concerning your eligibility and the conditions under which coverage is offered. We aim to simplify this aspect, providing clarity on how issue rights apply within the Medicare framework, ensuring you have the necessary insights to assess your healthcare choices effectively.

Are Medicare Advantage Plans Guaranteed Issue?

Key Highlights

- Medicare Advantage plans offer comprehensive coverage, combining hospital, medical, and often prescription drug services, and additional benefits.

- Guaranteed issue rights protect beneficiaries from medical underwriting when purchasing Medigap, ensuring uninterrupted access to coverage.

- Key differences exist between Medicare Advantage and Medigap: Advantage plans offer integrated benefits; Medigap supplements Original Medicare.

- Understanding enrollment periods is crucial for optimizing coverage options and avoiding penalties or gaps in healthcare access.

- Tools like MedicarePartCPlans.org assist beneficiaries in comparing plans based on personal healthcare needs and financial circumstances.

Compare plans and enroll online

Understanding Medicare Advantage Plan Basics

Medicare Advantage plans offer an alternative to traditional Medicare by providing comprehensive coverage that combines hospital, medical, and often prescription drug services. These plans are becoming increasingly popular among Medicare beneficiaries because they often include additional benefits like vision, dental, and wellness programs. In understanding the various aspects of Medicare Advantage, it’s important to explore what these plans entail and the diverse types available to meet varied healthcare needs. Recognizing these elements will empower you to make informed decisions about the healthcare coverage that best suits your circumstances.

What is a Medicare Advantage Plan?

A Medicare Advantage plan, also known as Medicare Part C, is a health insurance plan offered by private companies that have a contract with Medicare to provide Part A and Part B benefits. Many Medicare Advantage plans also include additional benefits such as vision, dental, and prescription drug coverage, which is not covered under traditional Medicare. These plans must follow rules set by Medicare, but they can charge different out-of-pocket costs and have different rules for how you get services, like whether you need a referral to see a specialist or if you must stay within network providers for non-emergency or non-urgent care.

Medicare Advantage plans are required by law to provide at least the same level of coverage as traditional Medicare, including hospital and medical insurance, but many offer added benefits. Beneficiaries choose Medicare Advantage plans because they can bring together various healthcare services under a single plan, often simplifying management of their medical care. These plans can be inexpensive or even include no additional premiums beyond what you pay for Medicare Part B, but this isn’t always the case. Be sure to evaluate each plan’s details to find the one that balances costs with coverage for your unique needs.

With enrollment periods being specific and certain rules governing switching from and to these plans, it’s crucial to understand the parameters set forth by Medicare. You will want to pay close attention to the Annual Election Period and the Open Enrollment Period when it comes to Medicare Advantage, as they determine when you can join or change plans. Moreover, Medicare beneficiaries have the chance each year to review their current Medicare Advantage plan options and make a change if desired without losing coverage.

The key here is knowing your healthcare requirements and selecting a plan that not only complements those needs but also fits within your financial plans.

Different Types of Medicare Advantage Plans

Medicare Advantage plans come in various forms, tailored to meet the diverse healthcare needs of beneficiaries. The most common types include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Private Fee-For-Service (PFFS) plans, Special Needs Plans (SNPs), and Medicare Medical Savings Account (MSA) plans. Each type of plan comes with unique structures regarding provider networks, cost-sharing relationships, and flexibility in service access, all designed to cater to different healthcare and lifestyle preferences.

HMO plans typically require members to receive care through a network of doctors and hospitals. These plans often emphasize preventive care and wellness, maintaining lower costs by restricting the choice of providers. In contrast, PPO plans offer more flexibility, allowing members to see any doctor or specialist but generally at a higher cost if they choose an out-of-network provider. This suits those who want the freedom to seek care from a larger pool of medical professionals.

PFFS plans, on the other hand, determine how much they will pay for a service and what you must cover at the point of service. You may visit any Medicare-approved doctor who agrees to accept the plan’s payment terms and conditions. These plans often appeal to beneficiaries who want flexibility and are willing to pay more at the point of service for that choice.

Special Needs Plans are crafted specifically for defined populations such as individuals with chronic conditions, institutionalized individuals, or dual eligibles who qualify for both Medicare and Medicaid. SNPs tailor benefits, provider choices, and drug formularies to best meet the specific needs of the groups they serve, offering highly personalized care.

Finally, MSA plans combine high-deductible insurance plans with bank accounts to pay for covered healthcare services, offering a way to set aside money specifically for healthcare expenses.

While these plans require careful management of healthcare spending, they are suitable for beneficiaries who prefer having savings reserved for health-related costs.

Choosing the right Medicare Advantage plan involves not just understanding what each plan type offers but also matching those offerings to personal health needs and financial circumstances. It’s essential to review the specifics of each plan, consider provider networks, out-of-pocket costs, and any additional benefits offered, and ensure alignment with both current health needs and financial situation.

Remember, this choice not only affects your healthcare access but can also impact long-term health management and financial planning. Use resources like the Medicare plans finder tool on our website to compare your options efficiently and make the best-informed decision about your healthcare coverage.

Exploring Guaranteed Issue Rights

Guaranteed issue rights are vital protections ensuring Medicare beneficiaries can secure Medigap policies without enduring probation due to pre-existing conditions or other requirements. These rights typically arise during certain enrollment periods, offering an essential safety net for switching or acquiring coverage. Understanding when and how these rights apply helps Medicare recipients make informed decisions, protecting their access to necessary medical services. As we navigate the complexities of guaranteed issue rights, it’s crucial to recognize their importance in safeguarding seamless healthcare transitions through comprehensive coverage options.

What Are Guaranteed Issue Rights?

Guaranteed issue rights are provisions that allow Medicare beneficiaries to purchase a Medigap policy without medical underwriting. This means insurers are required by federal law to offer coverage regardless of health status, requiring insurers to provide the plan without the need for a medical history review. Such rights come into play primarily when certain conditions are met, such as losing other health coverage or during specific enrollment periods, significantly contributing to the stability of healthcare access for older adults.

Coverage remains uninterrupted as long as the Medigap policy is purchased during these periods. It’s a crucial element in Medicare Part C, often misunderstood, leading many people to miss out on benefits potentially essential to their healthcare planning.

The significance of guaranteed issue rights is rooted in the protection they afford against possible denials due to pre-existing conditions, ensuring continuous access to healthcare services. While most often associated with the Medigap open enrollment period, which is a one-time six-month window that begins when you turn 65 and enroll in Medicare Part B, these rights also activate under specified circumstances, such as loss of employee-based health coverage. Knowing these rights can spare beneficiaries from the distress of navigating healthcare transitions without adequate insurance, particularly valuable for those with ongoing medical needs.

Medicare Insurance offers a broad spectrum of plans, yet understanding how guaranteed issue rights interlace with Medicare policies can smooth the selection process, allowing for seasoned navigation through a complex landscape of choices. Since these rights essentially protect choice and access, it’s paramount for Medicare beneficiaries to be aware of them.

Accessing a Medigap policy through these rights emphasizes the ethos of Medicare: providing comprehensive, adaptable, and secure healthcare coverage for older individuals. This assurance aids beneficiaries in planning their health expenses without fear of unexpected denials or increased costs, underpinning the foundational principle of Medicare as a reliable support system.

| Right Type | Eligibility Criteria | Coverage Start | Plan Options | Key Benefits |

|---|---|---|---|---|

| Initial Enrollment | During the first 6 months of Medicare Part B enrollment | Immediately upon sign-up | A variety of Medigap plans are available | No health questions required |

| Trial Right | First time in a Medicare Advantage Plan, within the first year | Return to Original Medicare within the first year | Access to the previous Medigap plan | Protection for trying a Medicare Advantage plan |

| Special Circumstances | Involuntary loss of other health coverage | Within 63 days of losing previous coverage | Choice of any Medigap plan available | Ensures continuity of coverage |

| Geographic Relocation | Moving out of the plan’s service area | Upon move or within 63 days | Available plans in the new area | Maintains coverage upon relocation |

This table highlights how these rights seamlessly integrate with and support the goals of Medicare by providing crucial protections for recipients.

When Do Guaranteed Issue Rights Apply?

Guaranteed issue rights apply under several specific circumstances, which are critical for Medicare beneficiaries to understand in order to maintain their Medigap eligibility and avoid coverage gaps. The most common scenario is during the open enrollment period, which gives individuals a dedicated timeframe to enroll in any basic Medigap policy available in their area without worrying about exclusions for pre-existing conditions. During this crucial period, insurers cannot charge more based on health conditions, ensuring fair access to Medicare policies when beneficiaries are most vulnerable to changes.

When discussing when these guaranteed issue rights apply, it’s essential to consider changes in coverage due to circumstances like losing Medigap or Medicare Advantage plan coverage. If your plan changes its area of service or discontinues its operations, you’ll typically qualify for guaranteed issue rights, protecting your access to alternative coverage. This is equally applicable when coverage ends because of moving to a different state where your plan is unavailable. These situations demand swift actions to ensure that the transition between policies remains smooth and without lapses, underlining the rights as cornerstones of secure Medicare transitions.

Life events, such as employer group health plan termination and ending a trial period in a Medicare Advantage plan, also evoke guaranteed issue rights. Specifically, if you change from traditional Medicare to an Advantage plan and decide within a year that it’s not the right fit, you’re entitled to revert and secure a Medigap policy. This trial period is invaluable for those trying Medicare Advantage for the first time, allowing a risk-free assessment of its benefits versus traditional Medicare with Medigap. Understanding these events can significantly help beneficiaries avoid being blindsided by sudden coverage needs.

Finally, federal law extends these rights to ensure that insurers can’t terminate your coverage due to health underperformance or discriminatory reasons, which significantly strengthens the Medicare framework. Each state may impose additional regulations enhancing these protections, thus necessitating a keen awareness of both federal and state-specific provisions.

Armed with the knowledge of when guaranteed issue rights apply, beneficiaries can confidently anticipate and manage Medicare policy transitions. For personalized assistance, tools available on resources like MedicarePartCPlans.org serve to simplify the understanding and application of these rights, assisting beneficiaries in maintaining optimal healthcare coverage.

Find & Compare Plans Online

Comparing Medicare Advantage and Medigap Policies

Choosing the right healthcare coverage involves understanding the differences between Medicare Advantage and Medigap policies. Each presents unique advantages and potential drawbacks, depending on your health needs and financial situation. While Medicare Advantage plans integrate Medicare Part A and B with potentially added benefits, Medigap policies supplement Original Medicare by covering additional costs. Familiarizing yourself with these distinctions can empower beneficiaries to make sound decisions about health coverage that aligns with their needs. Let’s explore Medigap insurers, eligibility, and how guaranteed-issue Medigap policies can work for you.

Medicare Advantage vs Medigap: Key Differences

When navigating the landscape of Medicare coverage, understanding the core differences between Medicare Advantage and Medigap policies is crucial. Medicare Advantage plans, often called Medicare Part C, are offered by private companies and include all benefits covered under Original Medicare Part A and Part B, plus often additional coverage like vision, dental, and prescription drugs. These plans contract with Medicare to provide these benefits and usually come with specific network rules, similar to employer health insurance, where you may need referrals to see specialists or be restricted to network providers unless it’s an emergency or urgent care case.

Medigap, commonly known as Medicare Supplement Insurance, is a different type of policy entirely. It’s not a standalone plan like Medicare Advantage but rather an addition to Original Medicare. This means when you choose a Medigap policy, you’re staying with traditional Medicare. The purpose of a Medigap policy is to help cover some of the costs not included in Original Medicare, such as copayments, coinsurance, and deductibles. Some Medigap policies might even cover services that Original Medicare doesn’t include, like medical care when you travel outside the U.S.

A significant consideration when choosing between Medicare Advantage plans and Medigap policies is the coverage network and cost structure. Advantage plans may offer lower initial or even no additional premium costs, but could result in higher out-of-pocket costs, especially if you go outside the provider network. These plans often operate like traditional HMO or PPO plans, providing incentives for using in-network healthcare providers. On the other hand, Medigap policies generally come with higher monthly premiums but can offer more predictable out-of-pocket costs, as they cover a larger portion of services that Original Medicare doesn’t fully pay.

Another difference lies in the flexibility of services. Medicare Advantage plans often require enrollees to use plan-specific networks for non-emergency care, while Medigap policies allow for a broader choice of providers since they’re paired with Original Medicare. Beneficiaries shopping for coverage must consider personal health needs, financial circumstances, and the stability of provider access. It’s also vital to be aware of how federal laws and state regulations impact the choices available, specifying particular rules for enrollment periods and the rights to secure Medigap insurance without undergoing medical underwriting in the initial enrollment phase.

The decision between a Medicare Advantage plan and a Medigap policy ultimately hinges on personal needs and preferences. Those who appreciate having comprehensive healthcare management under one package might favor an Advantage plan, while those valuing flexibility and ease of budgeting Medicare-related expenses could find Medigap supplements more appealing. Using resources like the Medicare plans finder tool on MedicarePartCPlans.org ensures that beneficiaries can compare policies effectively by location and needs, facilitating a well-informed decision that can maintain or improve health outcomes while managing costs effectively.

To further assist in navigating the differences, consider these additional points that highlight key considerations when choosing between these plans:

- Evaluate your need for routine vision and dental care.

- Consider travel frequency and coverage needs outside the U.S.

- Assess your comfort with network restrictions.

- Examine your typical healthcare usage versus premium costs.

- Look at the potential for variable out-of-pocket costs annually.

- Review available resources like Medicare.gov tools.

These insights can guide your exploration, ensuring you align your healthcare choices with personal needs and financial goals.

How Guaranteed-Issue Medigap Policies Work

Guaranteed-issue Medigap policies are critical for Medicare beneficiaries, particularly when transitioning from other forms of coverage or when encountering certain life changes. Medicare beneficiaries who opt for Medigap policies within specific timeframes can leverage these guaranteed-issue rights, ensuring they receive coverage without being subject to medical underwriting processes that could deny coverage due to pre-existing conditions. Federal law mandates that insurance companies offering these Medigap policies must provide coverage without increased premiums due to health status, safeguarding essential healthcare continuity for older adults.

The guaranteed-issue rights typically come into play during the Medigap open enrollment period, a six-month window that starts when you enroll in Medicare Part B. During this period, you’re eligible to purchase any Medigap policy in your area without health evaluations. Though open enrollment is the most widely known time for these rights, other specific circumstances also apply. For instance, if a beneficiary loses Medicare Advantage coverage due to plan service area changes or discontinuation, these rights activate, allowing them to safely transition to Medigap without insurance rejections due to their medical condition.

Another scenario where guaranteed-issue rights apply includes the expiration of a trial period with a Medicare Advantage plan. Beneficiaries moving from traditional Medicare to an Advantage plan are given a one-year grace to revert back if the plan does not meet their expectations or needs. Within this period, they can secure a Medigap policy upon returning to Original Medicare coverage. This flexibility is vital, enabling cautious evaluation of a new plan that aligns with their healthcare management philosophy.

The interaction of federal law and individual state regulations deepens the complexity of guaranteed-issue rights. Some states extend additional protections beyond federal law, adding another layer of security for those eligible for Medicare. This includes allowing guaranteed-issue rights in other circumstances, like when losing employer group health coverage. Being aware of state-specific guidelines fortifies beneficiaries in their negotiation of the complex Medicare landscape, structuring a more predictable and equitable coverage experience.

Ultimately, understanding how these rights work not only informs strategic health coverage choices but also ensures beneficiaries are prepared to adapt to changes in health plans as needed without fear of coverage gaps or denied claims. Utilizing tools and guidance available through resources like MedicarePartCPlans.org can greatly aid beneficiaries in identifying the best timing and strategy to use these invaluable rights. For those navigating Medicare transitions or exploring extended coverage options, such comprehensive guidance entrenches their assurance of sustained health care access.

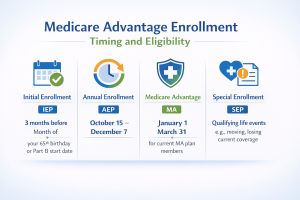

Navigating Medicare Enrollment Periods

Understanding Medicare enrollment periods is essential in optimizing healthcare coverage. These periods include critical windows when you can make changes to your Medicare Advantage and Medigap policies without penalty. The process involves knowing terms like open enrollment and trial periods, key for making informed decisions about your insurance needs. This section delves into these specific timeframes, ensuring you maximize your coverage options and safeguard access to necessary services. As you navigate these periods, insights into state-specific regulations and insurers’ requirements will be crucial to maintaining uninterrupted healthcare access.

Understanding the Issue Period for Enrollment

The issue period for enrollment in Medicare-related plans is a pivotal time for beneficiaries, deeply impacting their choice of medical coverage and potential costs for the foreseeable future. The primary enrollment window, known as the Medigap open enrollment period, is key for Medicare beneficiaries looking to secure Medigap coverage. This six-month period begins when you enroll in Medicare Part B, providing a unique opportunity to purchase Medigap policies without the risk of medical underwriting, ensuring you aren’t denied coverage or charged higher premiums due to pre-existing conditions.

During this open enrollment window, insurance companies are mandated to sell you any plan they offer in your area, regardless of your health status. This offers a level of security and peace of mind, knowing that your choice of coverage at this time won’t come with unexpected health-related surcharges. This enrollment period is designed to coincide with when you first become eligible for Medicare, usually at age 65, aligning with when most individuals experience significant shifts in healthcare coverage needs.

Understanding the intricacies of this period is crucial. While it primarily speaks to Medigap policies, knowing about trial periods can also be beneficial if you are considering Medicare Advantage plans. A trial period allows you to try a Medicare Advantage plan but return to Original Medicare and a Medigap policy within 12 months if it doesn’t meet your needs. This trial period offers a buffer for making informed comparisons between Medicare Advantage and Medigap policies, helping to ensure that the coverage you choose aligns with your healthcare requirements and lifestyle preferences.

State-specific variations can further complicate this enrollment landscape, with some states offering more robust protections or additional rights beyond the federal guidelines. As regulations can differ significantly from one state to another, it becomes important for beneficiaries to understand how their local laws impact their choices. In some cases, states impose additional requirements to guarantee insurers provide fair and comprehensive coverage options during the Medigap open enrollment period.

Knowing these conditions enables informed decision-making and offers a safeguard against potential missteps that could affect long-term healthcare access and costs.

Furthermore, recognizing the implications of your policy choices during this period can have lasting effects on your eligibility for future coverage adjustments and on your overall healthcare costs. Engaging with resources like MedicarePartCPlans.org equips beneficiaries with the tools to analyze available plans and understand the influence of each enrollment period on coverage decisions. This proactive approach is essential for securing the medical coverage that best fits your health and financial needs as you move forward into your Medicare years.

In summary, comprehending the concept of issue rights is crucial for selecting a Medicare Advantage plan. These rights play a significant role in coverage options, especially under specific circumstances like losing other healthcare coverage or moving. Always explore your options thoroughly, considering personal healthcare needs and budget. Utilize resources such as MedicarePlanCPlans.org to compare plans effectively. By doing so, you can make informed decisions to ensure comprehensive healthcare coverage tailored to your requirements.

Compare plans and enroll online

Frequently Asked Questions

What is a Medicare Advantage Plan?

A Medicare Advantage Plan, or Medicare Part C, is an alternative to traditional Medicare offered by private insurance companies. These plans provide coverage for Part A and Part B benefits and often include additional benefits like vision, dental, and prescription drugs.

How does a Medicare Advantage Plan differ from a Medigap policy?

Medicare Advantage plans combine multiple healthcare services under one plan, while Medigap policies supplement Original Medicare by covering additional costs like copayments and deductibles. Advantage plans often require network providers, whereas Medigap policies typically allow more provider flexibility.

What are issue rights and how do they apply in Medicare?

Issue rights enable Medicare beneficiaries to secure Medigap policies without undergoing medical underwriting. These rights are particularly important during specific enrollment periods or when switching coverage, ensuring uninterrupted access to healthcare services.

When is the Medicare enrollment period?

Medicare has several enrollment periods, including the Initial Enrollment Period, the Annual Election Period, and the Medigap Open Enrollment Period. These periods allow beneficiaries to enroll in, change, or drop plans. Specific rules govern each period, impacting coverage and potential penalties.

How can I compare Medicare Advantage plans?

To compare Medicare Advantage plans, you should consider coverage options, costs, and benefits. Tools like those provided by MedicarePartCPlans.org can help you evaluate different plans based on your healthcare needs and financial circumstances.

Have Questions?

Speak with a licensed insurance agent

1-877-436-2343

TTY users 711

Mon-Fri: 8am-9pm ET

Find & Compare Plans Online

ZRN Health & Financial Services, LLC, a Texas limited liability company