The Medicare Part C Plans Finder Tool is an invaluable resource for anyone looking to navigate the complexities of Medicare Advantage plans, commonly known as Part C. This online tool is designed to help beneficiaries understand their options by providing detailed comparisons of available plans within their geographic region. As you journey through the selection of your Medicare Advantage plan, leveraging this tool can save you time and confusion by consolidating essential information in one accessible place.

Using the Medicare Part C Plans Finder Tool is straightforward, yet incredibly thorough. Begin by entering your ZIP code and any pertinent personal details, such as your Medicare eligibility and current level of healthcare needs. The tool then compiles a list of available Advantage plans in your area, highlighting each plan’s coverage details, insurance company, premium costs, and out-of-pocket expenses. By providing a clear view of what’s available, it allows beneficiaries to align plans with their specific hospital and medical needs, including prescription drug coverage and additional benefits like dental or vision care.

For those eligible for Medicare, particularly adults aged 60 to 85, the tool offers a chance to compare year-round options at a glance without enrolling prematurely. It assists in identifying the criteria important for making informed choices, such as network providers and plan copayments. This is crucial during the Medicare Advantage enrollment period, where understanding policy nuances can affect the overall satisfaction with insurance. For instance, by knowing whether your preferred doctors or hospitals are in-network, you can avoid unexpected medical costs or inconvenience.

Moreover, the tool provides insight into the annual changes occurring in Medicare Advantage plans. This is particularly useful during open enrollment periods where policy updates are prevalent. Beneficiaries can stay informed about modifications in drug coverage, adjustments in plan coverage areas, and even changes in premiums. With this knowledge, you can make proactive decisions about enrolling in a different Medicare Advantage plan or renewing an existing one.

Beyond just data, the Medicare Part C Plans Finder Tool offers a sense of control over your healthcare future. By empowering you to make educated choices, you can ensure that your Medicare Advantage plan reflects your personal health priorities, financial situation, and eligibility requirements. It serves as a bridge to the broader Medicare.gov landscape, making it easier to access official information without feeling overwhelmed by professional jargon or complex policy language.

In essence, using the Medicare Part C Plans Finder Tool is about facilitating a more engaging and less perplexing experience when joining or switching to a Medicare Advantage plan. It supports informed decision-making by tailoring the search to each user’s unique circumstances, whether you’re just starting your Medicare journey or reassessing your ongoing needs.

For caregivers aiding family members in choosing coverage options, it simplifies the coordination effort by summarizing potential policy choices in an easy-to-digest format. The convenience and insights it offers are invaluable assets in ensuring that you or your loved ones receive the optimal coverage and care required in the golden years.

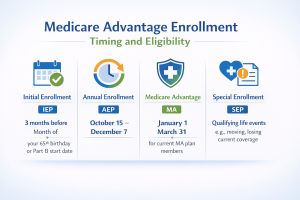

Navigating Medicare Advantage enrollment can seem complex, but understanding key enrollment periods allows you to make informed choices. Being aware of times like the Initial Coverage Election Period, Annual Election Period, and Special Enrollment Periods can guide your decision-making process. Familiarize yourself with these timelines to determine if changes in your circumstances allow for plan adjustments. Our resources at MedicarePartCPlans.org aim to clarify your options and assist you in evaluating coverage that aligns with your healthcare needs. For personalized help, visit our website to explore our plan finder tool and ensure your Medicare goals are met.