When navigating Humana Medicare plans, understanding the nuances between copays and coinsurance is essential for effectively managing out-of-pocket healthcare costs. While both terms involve sharing costs with the insurer, copays are fixed amounts paid for specific services, such as doctor visits or prescriptions, whereas coinsurance is a percentage of the cost for covered services. This distinction can impact your healthcare budgeting and choices. In this guide, we will break down copays and coinsurance details to help you make informed decisions about your Humana Medicare plan options, ensuring clarity and confidence in your healthcare journey.

Copays and Coinsurance in Humana Medicare

Key Highlights

- Copays provide predictable costs for specific services, while coinsurance requires paying a percentage of service costs.

- Medicare Advantage plans might include extra benefits like vision, hearing, and prescription drug coverage beyond Original Medicare.

- Understanding coinsurance helps control out-of-pocket expenses, especially for high-cost or frequent services.

- Choosing in-network providers within Medicare Advantage plans can lead to lower copay and coinsurance costs.

- Utilizing resources like MedicarePartCPlans.org aids in comparing plans and understanding cost-sharing methods effectively.

Compare plans and enroll online

Introduction to Medicare and Its Parts

Medicare is a vital program providing health insurance to millions of American seniors, helping them access essential health services. Understanding Medicare and its various parts, Original Medicare, Medicare Advantage, Medigap, and more, is crucial for making informed coverage choices. This section unpacks Original Medicare and explores the advantages of Medicare Advantage plans, helping beneficiaries navigate their options effectively.

Understanding Original Medicare Coverage

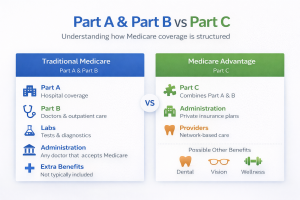

Original Medicare, encompassing Part A and Part B, is the cornerstone of the Medicare program. Part A typically covers inpatient hospital services, skilled nursing facility care, hospice, and some home health services. It primarily takes care of inpatient stays and associated healthcare needs. On the other hand, Part B handles outpatient care, covering medical services like doctor visits, preventive services, ambulatory services, and necessary medical supplies needed for a range of health conditions. Together, Parts A and B provide foundational health insurance coverage that is vital for eligible seniors navigating their healthcare journey.

Original Medicare operates under a system where beneficiaries can visit any doctor or healthcare provider that accepts Medicare, across the United States. This flexibility ensures expansive network access, which is a significant advantage for those frequently traveling or living in multiple locations throughout the year. However, understanding this coverage is critical, as it doesn’t pay for everything. Many beneficiaries learn that out-of-pocket expenses such as deductibles, copays, and coinsurance can accumulate under Original Medicare, especially without supplemental plans.

Original Medicare operates within a structured fee-for-service model, and the Medicare-approved amount dictates what services cost. Beneficiaries typically pay a portion of this cost, whether it’s a deductible or a percentage under coinsurance. Although Original Medicare covers a wide array of services, like inpatient and outpatient care, there are notable exclusions such as prescription drugs, dental care, vision, and hearing aids. This gap in coverage often motivates Medicare beneficiaries to explore supplementary options like Medicare Advantage plans or Medigap policies that can mitigate some of these additional costs.

It’s crucial to review your health needs regularly and not only rely on Original Medicare’s standard coverage. By doing so, you ensure that you’re receiving adequate coverage that’s aligned with your health situations. Engaging with resources like Medicare.gov and trusted educational platforms such as MedicarePartCPlans.org can provide insights and updates on any changes affecting coverage and help guide decisions concerning health insurance services.

The Role of Medicare Advantage Plans

Medicare Advantage plans, also known as Medicare Part C, offer a bundled alternative to Original Medicare. These plans are provided by private insurance companies approved by Medicare and include Parts A and B coverage while often adding extra benefits not routinely covered by Original Medicare. One notable aspect of Medicare Advantage plans is the additional coverage options they may offer, such as vision, hearing, dental, and even wellness programs, giving beneficiaries a more holistic approach to healthcare.

Due to their network-based structure, Medicare Advantage plans often work similarly to traditional health maintenance organizations (HMOs) or preferred provider organizations (PPOs). This setup means that beneficiaries might have to choose healthcare providers within a specific network to get the lowest costs, but it allows for a more managed care experience tailored to their individual health needs. Another advantage is that many Medicare Advantage plans include prescription drug coverage under Medicare Part D, which can simplify how beneficiaries manage their health services and medicine needs under one policy.

While the scope of coverage under Medicare Advantage plans is broad, understanding the different plan options is crucial, as each insurance company provides diverse benefits and services. Various plans may offer unique supplemental benefits that are ideal, like transportation services, memberships to fitness programs, or access to telehealth services, reflecting the plans’ flexibility to adapt to modern healthcare landscapes.

For those seeking a comprehensive coverage package, Medicare Advantage can be a compelling option. But choosing the right Medicare Advantage plan requires careful consideration of your healthcare needs and preferences. Utilizing tools provided by platforms like MedicarePartCPlans.org can be beneficial for reviewing and comparing available Advantage plans by coverage and location. As plans vary significantly by region, it’s essential to understand the specific costs, coverage options, and provider networks available in your area to make a well-informed decision about your health insurance coverage.

What is a Copay?

A copay, or copayment, is a fixed payment amount that a Medicare beneficiary pays out-of-pocket when receiving specific healthcare services. This concept is a vital part of understanding how Medicare Advantage plans and other health insurance models work. Unlike coinsurance, where costs are shared as a percentage, copays are predetermined amounts set by the insurance company, ensuring predictability in certain healthcare expenses. This section explores how copays function within Medicare plans, helping beneficiaries comprehend how these fixed costs impact their overall out-of-pocket expenses.

Understanding Copays in Medicare Plans

Understanding copays is crucial when navigating Medicare plans. A copay is a flat fee you pay for a specific service or prescription, and it’s typically required at the time of service. Medicare Advantage plans, offered by private insurance companies, frequently incorporate copayments into their coverage structure. This approach allows enrollees to pay a reduced, set amount for services such as doctor visits, prescription drugs, or specialist appointments, making healthcare costs more predictable. For example, with Medicare Part C, a plan might require you to pay a $20 copay each time you visit your primary care physician.

In the context of Medicare, copays can vary greatly depending on the services and the specific Medicare Advantage plan chosen. It’s important for enrollees to thoroughly review their plan details, as copays for specialist visits, hospital stays, or prescription drugs might differ significantly. A copay is generally lower for a primary care physician visit than for seeing a specialist. This structure helps manage out-of-pocket costs while encouraging beneficiaries to utilize necessary healthcare services proactively.

Medicare Advantage, also known as Medicare Part C, often includes prescription drug coverage, where copays come into play for purchasing medications. For many plans, prescription drugs are categorized within tiers, and each tier has a different copayment amount. Lower-tier generic medications usually come with lower copays, while higher-tier or brand-name drugs may have higher copays. This tiered system is designed to incentivize the use of more cost-effective medications, ultimately impacting your out-of-pocket expenses.

The role of copays in Medicare is multifaceted. They’re a tool to help manage healthcare costs, ensuring beneficiaries contribute to their healthcare expenses without facing unexpected financial burdens. As copays are fixed, they are particularly beneficial for budgeting, as enrollees know ahead of time what their contribution will be for standard services. This predictability is especially helpful for those living on fixed incomes, common among Medicare beneficiaries. Understanding the details of copays in your plan can empower you to make informed decisions about enrolling in a Medicare Advantage plan that best fits your needs and budget.

How Copays Impact Your Out-of-Pocket Expenses

Copays significantly impact your out-of-pocket expenses by providing a level of predictability to your healthcare costs under Medicare plans. These fixed payments ensure that while you have some financial responsibility for the services you use, you’re shielded from the unpredictability of healthcare charges that can occur with other cost-sharing methods like coinsurance.

For those enrolled in Medicare Advantage plans, understanding copays in the context of out-of-pocket expenses is essential. Copays differ depending on the type of service or whether the service provider is within the plan’s network. For instance, visiting an in-network primary care doctor might incur a lower copay compared to consulting with a specialist or obtaining care out of network. This financial structure encourages beneficiaries to choose providers within the network, ensuring cost efficiency and giving more control over their medical expenses.

In addition to routine medical visits and specialist consultations, hospital stays can also involve copays when receiving healthcare through Medicare Advantage. Typically, beneficiaries might encounter copayments for each day they stay in an inpatient hospital. Understanding these costs upfront allows you to anticipate the impact on your household budget, particularly if you’re managing ongoing health issues that require frequent hospitalizations or medical attention.

Moreover, copays play a pivotal role in controlling pharmaceutical expenses, especially with Medicare Advantage plans that include prescription drug coverage. By offering fixed copayment amounts for medications, these plans provide clarity on drug costs, which is valuable for beneficiaries who rely on a stringent budget. This is particularly important considering how quickly medication expenses can accumulate, overwhelming those not fully prepared for variable costs.

Finally, copays encourage beneficiaries to seek necessary healthcare services without the fear of incurring prohibitive costs, as the predetermined payment model caps expenses for services like doctor visits, tests, or prescription medications. However, reaching your policy’s out-of-pocket maximum is possible, at which point copays and coinsurance may no longer be a requirement for the year. Understanding this aspect of your plan is essential for navigating and controlling overall health expenses effectively.

Leveraging resources and tools, such as those provided by MedicarePartCPlans.org, can offer clarity and assistance in comparing your available Medicare Advantage options, their copayment structures, and potential impacts on out-of-pocket expenses. This proactive approach ensures you’re equipped with the necessary knowledge to optimize your healthcare plan choice and management.

To further explore the influence of copays on your healthcare budgeting, consider the following aspects:

- Identify services covered under copay versus coinsurance for precise cost management.

- Examine copay differences between in-network and out-of-network providers.

- Anticipate costs with frequent healthcare needs impacting monthly budget allocations.

- Review copayment amounts for prescription drug plans under Medicare Advantage.

- Assess how copays can drive choices for necessary healthcare services.

- Recognize scenarios where the out-of-pocket maximum affects copay requirements.

- Utilize resources like MedicarePartCPlans.org for comprehensive plan comparison.

These points highlight key considerations for maximizing your understanding and control of copays and out-of-pocket expenses.

Find & Compare Plans Online

Exploring Coinsurance in Medicare

Coinsurance is a key element in understanding Medicare costs, as it affects how much beneficiaries pay for healthcare services after meeting their deductibles. Unlike copayments, which are fixed amounts, coinsurance requires paying a percentage of the covered costs. This section delves into the concept of coinsurance, examining how it fits into the Medicare framework and its implications for eligibility, coverage, and out-of-pocket expenses. By grasping the dynamics of coinsurance, Medicare beneficiaries can better navigate their options, especially when considering Original Medicare, Advantage plans, or supplemental insurance.

Coinsurance and Its Relation to Medicare Costs

Coinsurance plays a significant role in determining your out-of-pocket costs under Medicare. It refers to the percentage of costs you’re responsible for after meeting the deductible, which is the amount you must pay before your Medicare coverage begins to share costs. Within Original Medicare, for example, after meeting the Part B deductible, beneficiaries typically pay 20% coinsurance for medically necessary services covered by that part of the program. This 20% comes into play across a variety of services, including doctor visits and outpatient care, placing a cap on your financial responsibility whenever you’re accessing healthcare services, but still requiring careful budgeting from beneficiaries.

Medicare Advantage plans, offered through private insurance companies, may structure coinsurance differently compared to Original Medicare. These plans often have set coverages for specific services and offer varied cost-sharing arrangements, which can include both coinsurance and copays. The potential for these plans to cover additional health services, such as vision or prescription drugs, means that analyzing coinsurance for each service component becomes imperative. The benefit is in the opportunity for a more tailored coverage; however, the complexity of weighing coinsurance against overall benefits necessitates careful reading of plan details.

Coinsurances are especially common when dealing with prescription drug coverage. For those utilizing these benefits under Medicare Advantage plans, understanding how coinsurance affects medication costs is important. Typically, each medication falls under a tiered system, with some drugs incurring a high coinsurance percentage while others are more affordable. The intricate nature of these systems incentivizes beneficiaries to opt for generic or preferred medications to reduce their coinsurance charges.

Being mindful of coinsurance helps control healthcare expenses, especially for services not fully covered by Medicare. It encourages beneficiaries to remain engaged with their healthcare plans and routinely review their medical needs against their coverage options. Given that large medical expenses can unpredictably affect financial stability, understanding and planning for coinsurance can create a safety net. Resources like MedicarePartCPlans.org provide the tools to compare and understand these cost-sharing structures fully, facilitating more informed decisions regarding your healthcare coverage.

Examples of When You Might Encounter Coinsurance

Coinsurance is encountered in various aspects of Medicare services, influencing the way beneficiaries pay for healthcare. For instance, in an inpatient hospital setting, once you meet your deductible, you might face coinsurance for extended stays. Every day after the 60th in a benefit period can lead to coinsurance payments under Parts A and B, where Original Medicare prescribes a percentage the beneficiary must cover. This cost-sharing model dictates that understanding hospital coinsurance liabilities is crucial for planning long-term or unexpected hospital admissions, where costs can escalate swiftly.

Outpatient services present another area where coinsurance is prevalent. Services like specialist visits, outpatient surgery, or even mental health counseling under Medicare Part B are often subject to coinsurance. Beneficiaries typically pay 20% of the Medicare-approved amount after the deductible, creating clear incentives to weigh the necessity of services carefully and conservatively manage healthcare utilization. Moreover, should a beneficiary require high-cost services frequently, coinsurance obligations could accumulate significantly, prompting evaluation of plan supplemental options or Medigap policies for more predictable expense handling.

Additionally, coinsurance may come into play with durable medical equipment, such as wheelchairs or walkers, where a prescribed percentage of the costs must be covered by the beneficiary after meeting the deductible. Supplement plans might alleviate these pressures, but understanding the intrinsic setup of coinsurance for such items ensures preparation for these ongoing financial commitments.

Importantly, in the field of prescription drugs, coinsurance might be applicable at various stages, particularly for specialty medications under Medicare Advantage plans with prescription drug coverage. Often, high-tier drugs incur a significant coinsurance percentage, making initial costs steep for beneficiaries. The complexity of drug formulary tiers requires diligence in selecting medications that balance effectiveness with affordability. Knowing when you encounter coinsurances is vital for preparing financially, allowing beneficiaries to strategize healthcare decisions against budgetary constraints effectively. Utilizing calculators and plan comparison tools provided by MedicarePartCPlans.org can support these efforts, ensuring informed choices that align with individual healthcare needs and financial reality.

Comparing Copays and Coinsurance in Medicare

In the landscape of Medicare, understanding the financial intricacies of copays and coinsurance is pivotal for beneficiaries, particularly when choosing between Original Medicare and Medicare Advantage (Part C) plans. Both cost-sharing methods are essential for managing healthcare expenses, but they function differently. We delve into how these costs impact Medicare Advantage selections and why comprehending your plan’s specifics is crucial for informed healthcare decisions.

| Plan Type | Coverage Features | Network Options | Additional Benefits |

|---|---|---|---|

| Advantage HMO | Prescription drug coverage, vision, and dental | Requires use of in-network providers | Wellness programs, routine preventive services |

| Advantage PPO | Comprehensive coverage, including hearing and mental health services | Flexibility with both in-network and out-of-network care | Personalization options, fitness programs |

| Special Needs Plan (SNP) | Customized coverage for specific chronic conditions | Specified networks tailored to member health needs | Care coordination and specialized health services |

| Private Fee-for-Service (PFFS) | Varies by provider; often includes hospital and medical services | No formal network; providers must agree to plan terms | Programs supporting chronic care management |

This table encapsulates how understanding copays and coinsurance within Medicare Advantage plans is crucial for beneficiaries to navigate their healthcare costs effectively.

The Implications for Medicare Advantage Plans and Costs

Medicare Advantage plans, known as Part C, often feature a combination of copayments and coinsurance, shaping the way beneficiaries handle healthcare expenses. While copays are fixed amounts paid for services like doctor’s visits or prescription pickups, coinsurance requires a percentage of the total service cost after meeting deductibles. The implications of these payment systems within Medicare Advantage plans can profoundly affect your financial outlay, making it essential to understand how they integrate into your healthcare strategy.

One of the main advantages of copays in Medicare Advantage plans is the predictability they offer. When you’re aware of the exact out-of-pocket amount for each doctor visit, specialist appointment, or covered service, budgeting becomes more manageable. This certainty is crucial for Medicare beneficiaries, particularly those living on a fixed income, as it reduces the potential for unexpected expenses. Conversely, coinsurance introduces variability since it depends on the cost of the services you receive. While this can be daunting, it also means you might pay less for lower-cost services, saving money on inexpensive medical interventions.

The inclusion of prescription drugs in many Medicare Advantage plans further impacts how copays and coinsurance are managed. Most plans utilize a tiered system where generic drugs come with low copays and brand-name or specialty medications entail higher coinsurance rates. This tiered structure encourages the use of cost-effective prescriptions, potentially reducing your medical costs. However, navigating this requires a thorough understanding of your plan’s formulary and the associated tiers.

Network considerations also play a crucial role in determining copays and coinsurance effects. Medicare Advantage plans typically require adherence to specific provider networks. Visiting a doctor within your plan’s network usually results in lower copays or coinsurance, promoting cost efficiency. Out-of-network visits might incur higher costs, emphasizing the need to plan healthcare visits strategically to avoid steep expenses.

Overall, comprehending the implications of copays and coinsurance within Medicare Advantage plans is key to financial planning for healthcare costs. Tools like those provided by MedicarePartCPlans.org can help beneficiaries compare plan options based on these cost-sharing methods, equipping them with critical information to make educated choices about their healthcare coverage and manage potential expenses effectively.

Importance of Knowing Your Medicare Plan's Details

Understanding the specific details of your Medicare plan, including the nuances of copays and coinsurance, is crucial for navigating your healthcare coverage effectively. Each Medicare Advantage plan offers unique benefits and cost-sharing structures that can significantly impact your healthcare expenses and access to services. Delving into these details provides the insight needed to choose a plan that best meets your healthcare and financial needs.

First and foremost, reviewing your plan’s Summary of Benefits is vital. This document outlines all essential aspects of your plan, including copayment and coinsurance obligations for various services. It provides a clear picture of what you can expect when accessing healthcare services, helping you prepare financially. Additionally, understanding the coverage for prescription drugs in your Medicare Advantage plan is essential, as copays and coinsurances vary across drug tiers. Familiarizing yourself with your plan’s formulary can prevent unexpected costs when filling prescriptions.

Inpatient and outpatient care details are also crucial to understand within your plan. Each Medicare Advantage plan stipulates specific cost-sharing arrangements for hospital stays and outpatient services. Knowing these details can prevent surprises, especially if you require frequent healthcare services. For instance, some plans might require a daily copay for hospital stays, while others might define coinsurance percentages for outpatient procedures. By comprehensively understanding these aspects, you can strategize your healthcare utilization to optimize savings while retaining access to necessary services.

Another critical aspect to consider is the provider network associated with your Medicare Advantage plan. These plans typically work within defined networks, and accessing care outside of this network can lead to increased copays or coinsurance obligations. To mitigate costs effectively, beneficiaries should familiarize themselves with in-network providers and plan routine healthcare visits accordingly. This comprehension not only manages expenses but also helps ensure continuity of care by building relationships with providers.

To maximize these insights, leveraging resources like MedicarePartCPlans.org can be invaluable. This platform aids in comparing the breadth of Medicare Advantage plans, emphasizing the importance of thoroughly understanding cost structures, coverage limitations, and network requirements of each plan. By proactively engaging with these resources, beneficiaries can confidently select plans that align with their health needs and financial realities, enhancing their ability to navigate the complexities of Medicare coverage and secure their healthcare future effectively.

Understanding the nuances between copays and coinsurance in Humana Medicare plans is vital for managing healthcare expenses effectively. Copays provide a set cost for services, offering predictability in budgeting, while coinsurance involves paying a percentage of service costs, which varies based on usage. Being informed about these components can empower Medicare beneficiaries to make knowledgeable decisions aligning with personal financial and healthcare needs. Whether you are planning for an upcoming procedure or managing ongoing treatments, understanding these terms can help in navigating and optimizing your Medicare coverage effectively. Explore plan details and assess your healthcare priorities thoughtfully.

Compare plans and enroll online

Frequently Asked Questions

What is the difference between copays and coinsurance in Medicare plans?

Copays are fixed amounts paid for specific healthcare services, such as doctor’s visits or prescription drugs. Coinsurance, on the other hand, is a percentage of the cost for these services that beneficiaries pay after meeting their deductibles.

How do Medicare Advantage plans differ from Original Medicare?

Medicare Advantage plans, also known as Medicare Part C, are offered by private insurance companies and include all Part A and Part B benefits of Original Medicare, often with additional benefits like vision, dental, and prescription drug coverage.

What benefits can Medicare Advantage plans offer beyond Original Medicare?

Medicare Advantage plans can provide additional benefits such as vision, hearing, dental, and fitness programs. Many plans also include prescription drug coverage, unlike Original Medicare.

Why is it important to use in-network providers with Medicare Advantage?

Using in-network providers in Medicare Advantage plans often results in lower copayment and coinsurance costs, as these plans typically work within specific provider networks. Choosing in-network providers ensures cost-efficiency and helps avoid unexpected higher costs.

How can MedicarePartCPlans.org help when choosing Medicare plans?

MedicarePartCPlans.org offers comparison tools and resources to help beneficiaries understand different plan options, including cost-sharing methods, coverage specifics, and provider networks, assisting in making informed healthcare coverage choices.

Have Questions?

Speak with a licensed insurance agent

1-877-436-2343

TTY users 711

Mon-Fri: 8am-9pm ET

Find & Compare Plans Online

ZRN Health & Financial Services, LLC, a Texas limited liability company