Understanding Issue Age Medicare Supplement Plans is essential for making informed decisions about Medigap coverage. These plans, also known as Medigap policies, offer different premiums based on your age at the time of purchase. Navigating through the available options and plan choices can help beneficiaries identify the most suitable coverage for their healthcare needs. By exploring the nuances of these plans, including how costs can change over time, you can better assess which Medigap options align with your personal and financial circumstances, ensuring peace of mind as you enjoy your golden years.

Issue Age Medicare Supplement Plans

Key Highlights

- Issue age Medigap plans base premiums on the policyholder’s age at purchase, offering predictability in costs.

- Understanding Medicare parts and their integration with Medigap is vital for informed coverage decisions.

- Our free Medicare plans finder tool helps beneficiaries compare plan options by location and coverage needs.

- Issue age policies to avoid age-related premium hikes, beneficial for long-term financial planning.

- Medigap fills coverage gaps left by Original Medicare, reducing out-of-pocket expenses for enrollees.

Compare plans and enroll online

Understanding Medicare Parts and Their Relationship with Medigap

Navigating Medicare can feel like deciphering a complex map, but breaking it down into its core parts helps clarify your journey. Medicare consists of several parts, each covering different aspects of healthcare for beneficiaries. How these parts align with Medigap, also known as Medicare Supplement insurance, is crucial for making informed healthcare choices. Medigap plans serve to fill the gaps left by traditional Medicare, reducing out-of-pocket expenses for enrollees.

Understanding the symbiotic relationship between these Medicare parts and Medigap insurance can enhance your overall healthcare experience and help in comparing issue age Medicare Supplement plans.

| Medicare Part | Main Coverage | Cost Sharing | Interaction with Medigap |

|---|---|---|---|

| Part A | Hospital & Inpatient Care | Deductibles & Copayments | Medigap covers gaps in inpatient costs |

| Part B | Outpatient & Medical Services | Monthly Premiums, Copayments | Medigap helps cover Part B coinsurance |

| Part C (Medicare Advantage) | Combined Part A & B Benefits | Varies by Plan | Medigap not usable with Part C |

| Part D | Prescription Drugs | Annual Deductible, Monthly Premiums | Medigap doesn’t cover drug costs |

| Medigap | Secondary to Part A & B | Varies by Policy | Supplements Original Medicare, not Part D |

This table encapsulates how the different parts of Medicare and Medigap policies align to optimize health care coverage.

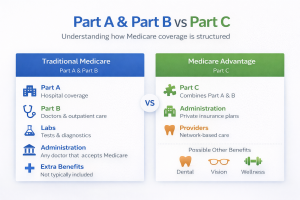

Key Medicare Parts Explained: A Basic Overview

Medicare is segmented into parts that cater to distinct aspects of health care, primarily designed to be comprehensive yet allow personalization through Medigap plans. The principal components include Part A (Hospital Insurance) and Part B (Medical Insurance), which together form what is known as Original Medicare. Part A typically covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care. On the other hand, Part B focuses on services and supplies that are considered medically necessary to treat a health condition.

This includes outpatient care, preventive services, ambulance services, and durable medical equipment. While Part A is often premium-free for most beneficiaries, Part B comes with a monthly premium, which is why many look to Medigap plans to alleviate additional costs.

Adding to the complexity, there’s Medicare Part C, or Medicare Advantage, which offers an alternative way to receive Medicare benefits. Medicare Advantage plans are provided by private insurers and often include additional benefits like dental and vision care. However, those using Medicare Advantage cannot pair their plans with Medigap, as these plans are structured differently. Finally, Medicare Part D covers prescription drugs and is essential for Medicare beneficiaries who require regular medication. Understanding these fundamental components is crucial for beneficiaries planning to optimize their health coverage with Medigap policies.

Medigap insurance, sometimes called Medicare Supplement insurance, specifically targets the gaps in Original Medicare by covering costs such as copayments, coinsurance, and deductibles. It’s important to note that Medigap plans do not work with Medicare Advantage plans but are instead only compatible with Original Medicare (Part A and Part B). Therefore, understanding each part of Medicare helps assess how Medigap insurance might best meet your healthcare expenditure needs, especially for those considering issue-age Medicare Supplement plans.

By grasping the essentials of each Medicare part and how Medigap complements them, beneficiaries can strategically enhance their coverage.

How Medicare Supplement Plans Integrate with Medicare Parts

Medigap insurance plays a pivotal role in augmenting the coverage provided by Original Medicare, easing the financial burden on beneficiaries. Medigap, or Medicare Supplement plans, are standardized policies offered by private insurance companies that specifically cover the “gaps” not paid by Medicare Parts A and B. These plans can cover expenses such as deductibles, coinsurance, and copayments, making healthcare costs more predictable for beneficiaries. Since Original Medicare does not fully cover all healthcare expenses, having a Medigap plan ensures that those gaps are efficiently bridged, significantly reducing out-of-pocket costs for beneficiaries.

When you enroll in a Medigap plan, you typically pay a monthly premium to the insurance company in addition to the Medicare Part B premium. It’s crucial to note that Medigap plans do not cover costs associated with prescription drugs, which is why many beneficiaries opt for a separate Medicare Part D plan to handle medication expenses. The integration of Medigap with Medicare Parts A and B is therefore chiefly concerned with enhancing coverage without duplicating benefits, allowing beneficiaries to have a more inclusive healthcare package.

Medigap policies come in different varieties, each offering a distinct level of benefits, yet every type must adhere to federal and state laws designed to protect beneficiaries. Importantly, each plan is identified by a letter (such as Plan F or Plan G), and not all plans are available in every location. Issue age Medigap plans, in particular, calculate premiums based on the age you are when you first buy the policy, which remains an influential consideration for many beneficiaries aiming to manage long-term healthcare costs.

Understanding how Medigap plans integrate seamlessly with Medicare Parts not only empowers you to make financially sound decisions but also supports a holistic approach to securing your healthcare needs.

Exploring Issue Age Medigap Insurance

Understanding how Medigap plan types, like issue age policies, operate can significantly impact long-term healthcare planning for Medicare beneficiaries. Issue age Medigap insurance bases its premiums on the age of policyholders when they first purchase the plan, potentially offering stability in your medical expenses as you age. This approach is distinct from other plan options, such as attained age or community-rated plans, making it crucial to grasp the nuances of issue age. By exploring these plans, you’ll gain insights into how they may align with your healthcare needs and financial expectations now and in the future.

What Is Issue Age Medigap Insurance and How Does It Work?

The issue age Medigap insurance is a specific type of Medicare Supplement policy where the premiums are determined by the age of the policyholder at the time of purchase. Essentially, the age you are when you buy your Medigap plan establishes the baseline for your premium costs. Unlike attained age policies, which increase in cost as you get older, issue age premiums generally remain stable with age, albeit they can still increase due to inflation and other external factors such as changes in healthcare costs or policy adjustments by your insurance provider.

The intrinsic appeal of issue-age Medigap policies lies in their predictability. Once your premium is set, you won’t experience the same age-related price hikes that often accompany other types of Medigap plans. This can be a crucial factor for Medicare beneficiaries who are keen on planning their healthcare expenses over the long term. Furthermore, by locking in your premium rate early, issue-age policies offer an element of financial stability, granting peace of mind as you budget for ongoing medical expenses while enjoying the comprehensive coverage these plans provide.

However, understanding this type of policy requires consideration of several factors. It’s important to note that while the age at which the policy is issued does set your initial premium, other market influences can cause the premium to rise. Health inflation, changes in insurance company policy, and general increases in healthcare costs can all affect the premiums for issue-age Medigap policies over time.

Thus, while your age at issue time stays constant, the market-related factors may still lead to a gradual increase in what you pay. Nevertheless, the main advantage remains the relative stability and the ability to avoid age-based hikes, which could prove beneficial for your financial planning.

Advantages of Issue Age over Other Medigap Policies

Issue age Medigap policies offer distinct advantages over other types, such as attained age or community-rated plans, particularly in their approach to calculating premiums. With issue age policies, as we’ve noted, premiums are based on the age when you first purchase the policy. This offers a significant benefit because it insulates you from premiums rising simply because you are getting older. This stabilizing factor appeals greatly to retirees, helping them manage their fixed incomes better across the years.

In comparison, attained age policies tend to start with lower premiums, but these premiums increase as you age. This can be problematic for long-term financial planning, as beneficiaries may face higher out-of-pocket costs as they enter advanced ages, when healthcare expenses might also naturally rise. On the other hand, community-rated policies don’t base premiums on age but on other factors, making them potentially less beneficial for individual pricing customization based on your specific life circumstances.

Therefore, the predictability of issue age Medigap plans can make them a compelling choice for many Medicare beneficiaries aiming for financial predictability.

Beyond just pricing, issue age policies can provide a sense of security due to their inherent premium stabilization. This aligns well with the needs of Medicare recipients who are planning for their healthcare by assessing costs over a series of decades rather than years. However, it’s crucial to be informed about the long-term implications and understand the slight increases that might occur due to inflation and increased healthcare provision costs, which are common to all Medigap policies regardless of type.

By evaluating these factors with a thorough understanding of your own healthcare needs, choosing an issue-age Medigap plan can indeed be a sound strategic move to ensure robust and cost-effective Medicare coverage.

Illinois Medigap Plans: Age Considerations and Premiums

Navigating Medigap options in Illinois requires an understanding of how age can influence premiums. Issue age Medigap plans and other policy types are shaped by various factors, impacting the cost of policies significantly. These plans help cover expenses not included in Original Medicare, reducing out-of-pocket costs for beneficiaries. Illinois residents must consider issue age Medigap policies alongside other rating systems, such as age-rated and community-rated policies, to find a suitable fit. By comprehending how these elements interact, beneficiaries can make informed decisions about their Medigap policies, ultimately securing comprehensive health coverage.

Find & Compare Plans Online

Illinois Issue Age Medigap Plans: Factors Affecting Premiums

In Illinois, the issue age Medigap plans base their premiums on the age you are when the policy is first issued. This is a crucial consideration for many Medicare beneficiaries, as it significantly impacts long-term healthcare costs. Unlike attained age policies where premiums escalate as you get older, issue age plans offer predictability by fixing your premium when you first purchase the plan. However, it’s important to be aware that factors such as inflation and changes in healthcare costs can still affect premiums over time, even if they’re not tied to your age increase.

One of the key benefits of issue age Medigap policies is the potential for financial stability. Since the premiums aren’t automatically adjusted upward with your age, beneficiaries in Illinois might find it easier to project and manage their healthcare expenses over the years. This aspect appeals particularly to those planning for retirement on a fixed income, where managing future costs is essential. Additionally, being aware of the specific terms and conditions of your Medigap policy, as outlined by your insurance provider, ensures you have a comprehensive understanding of any potential fluctuations.

For Illinois seniors exploring issue age Medigap policies, it’s also crucial to consider the broader spectrum of benefits provided. While the primary focus is often on the premiums, the robustness of coverage, including what Original Medicare Parts A and B don’t cover, should also be a priority. This includes potential costs like copayments, coinsurance, and deductibles. By evaluating both the cost and coverage areas, beneficiaries can effectively weigh their options and select a plan that aligns with their healthcare needs.

Moreover, understanding how Medigap plans complement the existing Medicare Parts is vital. Given that Medigap doesn’t replace Medicare but supplements it, knowing what gaps your issue age policy fills can facilitate better healthcare decisions. Policyholders in Illinois seeking comprehensive coverage through Medigap should engage with tools like the MedicarePartCPlans.org’s free Medicare plans finder to explore various plans tailored to their unique circumstances and geographical location, ensuring informed, cost-effective choices. This approach not only optimizes your financial planning but ensures your healthcare needs are adequately met.

A Comprehensive Look at Age Rated vs. Community Rated Policies

Age-rated and community-rated policies offer different mechanisms for determining Medigap premiums, playing a crucial role in how beneficiaries in Illinois manage their healthcare expenses. Age-rated policies are structured around your current age, meaning premiums typically start lower yet can increase significantly as you grow older. This tiered premium system might seem beneficial initially, but it can pose challenges for long-term financial planning, potentially leading to unexpectedly high healthcare costs in later years.

Conversely, community-rated policies take a different approach by offering a uniform premium for all policyholders within a specific area or community, regardless of their ages. This could be advantageous for those who favor predictability and don’t want their premium tied directly to aging. However, community-rated plans might not necessarily offer cost savings for everyone, as factors external to individual aging can also play into premium adjustments. This system’s reliance on a broader risk pool means that changes in policies or collective healthcare costs can affect everyone in the community uniformly.

Comparing these policies, it’s evident that each offers unique benefits that may cater to different financial strategies of Illinois Medicare beneficiaries. Issue age Medigap plans, discussed previously, attract those who prioritize lock-in premiums that do not naturally escalate just because policyholders are aging. While community-rated plans aid in providing averaged and potentially predictable premiums across a community, age-rated plans can initially offer lower starting points, albeit with the risk of rising drastically as one ages.

To make an informed decision between these Medigap policy types, Illinois seniors should assess their current financial situation and consider their healthcare plans’ long-term impact. It’s highly beneficial to utilize resources like MedicarePartCPlans.org, which offer a free Medicare plans finder tool. This tool assists beneficiaries in comparing these diverse policy types against their specific healthcare needs and financial objectives, ensuring a well-rounded approach to selecting a Medigap policy that offers the best predictability and coverage for their circumstances.

To further explore the nuances between age-rated and community-rated Medigap policies, consider the following key points:

- Age-rated plans might offer lower initial costs but can increase sharply with age.

- Community-rated plans provide consistent premiums across a given area, regardless of age.

- Factors such as collective healthcare costs can impact community-rated premiums.

- Issue age plans lock in premiums based on age at enrollment, avoiding age-based escalations.

- Consider long-term financial planning when choosing between policy types.

- Utilizing comparison tools can provide insights tailored to individual healthcare needs.

- Explore potential premium variations due to changes in community or healthcare policy conditions.

These points highlight essential considerations and strategies for evaluating Medigap policies.

Navigating Medigap Enrollment: Important Factors

Understanding the nuances of Medigap enrollment is essential for Medicare beneficiaries seeking to optimize their healthcare coverage. Medigap, as a complement to Original Medicare, involves a strategic enrollment process that demands careful consideration of several key factors. Among these, the type of Medigap plan and the impact of issue age are paramount. These elements not only influence your initial premium but also determine long-term healthcare costs. By delving into the steps and decisions involved in Medigap enrollment, beneficiaries can make informed choices that balance coverage needs with budgetary constraints.

Steps and Considerations in the Medigap Enrollment Process

Enrolling in a Medigap plan involves a series of steps that are crucial for ensuring appropriate healthcare coverage tailored to individual needs. The process begins with understanding the eligibility criteria. Generally, you’re eligible for Medigap if you’re enrolled in Medicare Part A and Part B. Timing your enrollment is particularly important. The best period to enroll is during your Medigap open enrollment period, which lasts for six months starting the month you turn 65 and are enrolled in Part B. During this window, you’re guaranteed the right to buy any Medigap policy sold in your state without the risk of being denied based on health status.

Once the timing is set, evaluating the different types of Medigap policies becomes the next vital step. Each plan, identified by letters, provides distinct coverage levels, with Plan F and Plan G being among the most comprehensive. However, Plan F is no longer available to new Medicare enrollees post-January 1, 2020. As you sift through your options, consider your current health needs as well as potential future medical issues, making sure your chosen plan can accommodate both. It’s important to recognize that not all plans are available in every state, so a location-based evaluation is necessary.

Another critical factor is comparing the overall cost of the plan, which includes both the monthly premium and out-of-pocket expenses not covered by Medigap. While issue age policies offer stable premiums based on the age you are when you first buy, other plans like attained age policies tend to increase premiums as you age. Community-rated plans, on the other hand, offer premiums that are not influenced by age. Weighing these cost structures against your long-term financial projections is crucial to making a sustainable choice.

Navigating the application process itself involves verifying the information on policy applications to ensure full accuracy, preventing potential future discrepancies in coverage. It’s also wise to consult resources and tools, such as the MedicarePartCPlans.org’s free Medicare plans finder, which can help compare available Medigap options by location and specific coverage needs. By carefully considering these steps and making informed decisions, beneficiaries can secure favorable Medigap policies that provide comprehensive coverage while meeting individual financial considerations.

Understanding the Effects of Issue Age on Enrollment Decisions

The choice between different Medigap plans heavily relies on how they factor in the issue age during enrollment, as this can significantly affect both current premiums and future financial stability. Issue age-rated policies establish premiums based on the age at which the policyholder first buys the plan. This means your premium remains stable in terms of your starting age, although it may still increase due to inflation or healthcare cost changes.

One of the major appeals of issue age policies is the predictability in premium costs over time. For beneficiaries planning long-term, the stability offered by these plans can be instrumental in managing retirement finances. Unlike attained age policies, which escalate in price as years go by, issue age plans circumvent age-related increases, allowing you to better predict your healthcare expenses. This can be particularly beneficial if you enroll in a Medigap plan at a younger age, locking in a lower premium than you might find with other policy structures.

Understanding how issue age plans differ from other types is crucial for making informed enrollment decisions. Attained age policies may appear less expensive initially, but they tend to catch up and surpass the cost of issue age policies as the policyholder ages, due to their increasing premium structure. On the other hand, community-rated plans offer a consistent premium across a community irrespective of age but might not always provide individual price benefits tailored to specific health needs or circumstances.

For Medicare beneficiaries, especially those retiring on fixed incomes, selecting an issue age policy might provide a financial strategy that aligns with their healthcare budgeting goals. The ability to avoid age-related premium hikes can offer peace of mind in planning for future expenses. However, it’s essential to consider all factors, such as location and available plans, to ensure comprehensive coverage. Leveraging tools like the free Medicare plans finder available at MedicarePartCPlans.org can greatly assist in comparing issue age policies against other options, ensuring a well-rounded decision that meets both healthcare coverage and financial needs.

Using MedicarePartCPlans.org to Find Suitable Medigap Options

Finding the right Medigap plan can be a complex task given the array of plans and types available, but MedicarePartCPlans.org aims to simplify this process. Our platform offers a free Medicare plans finder tool that empowers beneficiaries to compare Medigap options based on individual healthcare needs and geographic considerations. By leveraging this tool, users can surface nuanced details about issue age Medigap plans, understand premium structures, and explore how different policies can complement their Original Medicare coverage. The site is crafted to provide clear, unbiased insights, helping you navigate choices for more informed decisions.

How Our Free Medicare Plans Finder Tool Assists Your Search

The MedicarePartCPlans.org’s free Medicare plans finder tool is designed to be your guide in navigating the world of Medigap options, providing a streamlined, user-friendly service that takes the guesswork out of finding the most suitable plans. With a focus on clarity and utility, the tool allows Medicare beneficiaries to search for Medigap plans by entering their geographical location, ensuring that the options you are presented with take into account the specifics of your local market’s insurance offerings.

This means whether you’re interested in exploring issue age Medigap plans or any other policy type, you’ll have access to plans that are actually available to you, eliminating confusion and wasted effort.

When you begin your search using our tool, you’re not just looking at an array of plan types; you’re diving into a detailed comparison of how each plan can benefit you specifically, based on your age, community rating, and specific coverage needs. The tool breaks down the often complex insurance language into more digestible information, allowing you to easily understand how each plan works, including how issue-age Medigap policies might offer a strategic advantage when it comes to premium stability over time. By seeing how premiums are set and knowing which plans align with your financial scenario, you can make better choices regarding your healthcare.

Another critical feature of our tool is its comprehensive output on coverage differences. You can compare side-by-side what each plan covers in terms of gaps left by Original Medicare. For those leaning towards issue age policies, understanding how their initial premium is determined by their age at purchase, yet remains relatively stable, is crucial. This helps in setting realistic financial expectations and ensures stability as you age, without unexpected premium hikes. Moreover, the finder tool is adept in helping you anticipate these factors, presenting the big picture clearly.

Lastly, our Medicare plans finder supports informed decision-making by providing access to additional resources and guidance around Medigap enrollment. This includes understanding the best times to enroll and how state regulations might affect your options. The tool guides you through these nuances, offering insights into the importance of the initial enrollment period and how it can prevent being turned down for coverage or being charged higher premiums due to health concerns.

The benefit of using MedicarePartCPlans.org’s free plans finder tool is more than just ease of use; it is about the empowerment that comes with understanding your available choices in full. Whether evaluating issue age Medigap plans or comparing other Medigap types and options, this resource enables a more informed and strategic approach to selecting a plan that not only fills the gaps left by Medicare but fits seamlessly into your healthcare and financial plans as you age. This holistic approach to Medicare planning ensures you’re not just choosing an insurance policy; you’re making a strategic investment in your health and financial well-being.

Understanding the nuances of Issue Age Medicare Supplement Plans can greatly assist Medicare beneficiaries in making informed decisions about their healthcare coverage. By focusing on critical factors such as age, location, and personal health needs, individuals can find a suitable Medigap plan that aligns with their lifestyle and budgetary concerns. Keep in mind the importance of periodic reviews of your plan choices as personal and Medicare requirements may evolve. For personalized assistance, consider using resources like MedicarePartCPlans.org to efficiently compare different plan options available in your area and make educated choices confidently.

Compare plans and enroll online

Frequently Asked Questions

What are Issue Age Medicare Supplement Plans?

Issue Age Medicare Supplement Plans, also known as Medigap policies, are insurance plans where the premiums are determined by the age of the policyholder at the time of purchase. These plans are designed to offer more predictable costs over time.

How do Issue Age Medigap plans compare to other types of Medigap plans?

Issue Age Medigap plans base their cost on the age you are when you buy, providing more stable premiums over the years. In contrast, Attained Age plans increase premiums as you age, while Community-Rated plans offer the same premium for all policyholders in an area.

What is the relationship between Medigap and Original Medicare?

Medigap, also known as Medicare Supplement insurance, works alongside Original Medicare Parts A and B to help fill coverage gaps, such as copayments, coinsurance, and deductibles, reducing out-of-pocket expenses.

Can you use Medigap with Medicare Advantage plans?

No, Medigap plans cannot be used with Medicare Advantage plans (Medicare Part C). Medigap is designed to supplement Original Medicare only.

How can the MedicarePartCPlans.org tool help with Medigap plan selection?

The MedicarePartCPlans.org tool allows beneficiaries to compare Medigap options based on location and coverage needs, helping to identify plans that align with personal and financial circumstances.

Have Questions?

Speak with a licensed insurance agent

1-877-436-2343

TTY users 711

Mon-Fri: 8am-9pm ET

Find & Compare Plans Online

ZRN Health & Financial Services, LLC, a Texas limited liability company