When navigating Medicare options, understanding how costs like copayment and coinsurance influence your expenses is vital. UPMC Medicare plans incorporate both elements, impacting what you’ll pay for your healthcare services. This guide explores the nuances between copayments and coinsurance, offering a clear perspective on how these terms affect beneficiaries’ personal care expenditures. As you weigh your options and plan your healthcare budget, knowing the difference is critical to making informed decisions about your Medicare coverage with UPMC. Dive in to learn how these components shape your financial responsibility in healthcare services.

Copayment vs Coinsurance UPMC Medicare

Key Highlights

- Medicare Advantage (Part C) plans combine Part A and B, and may include Part D, offering comprehensive coverage.

- UPMC Medicare Advantage plans provide additional benefits like dental and vision, not covered by Original Medicare.

- Copayments are fixed charges per service, ensuring predictable costs and aiding in budget planning.

- Coinsurance involves shared percentages of medical costs, impacting overall healthcare expenses.

- Choosing the right plan requires evaluating copayments, coinsurance, and potential out-of-pocket costs.

Compare plans and enroll online

Introduction to Medicare Advantage Plans

Medicare Advantage plans, also known as Medicare Part C, offer an alternative way to get your Medicare benefits. These plans are provided by private insurance companies approved by Medicare and must cover all services that Original Medicare covers. However, they often include additional benefits, like dental, vision, and hearing coverage, and may have different rules, costs, and coverage restrictions.

As you look to understand Medicare Advantage plans’ unique offerings, it’s essential to understand their basic structure and how they differ from Original Medicare so you can make informed decisions.

Understanding the Basics of Medicare Advantage

Medicare Advantage plans, or Part C, integrate Medicare Part A (hospital insurance) and Part B (medical insurance) into a single health plan. They bring additional benefits not typically available with Original Medicare, such as dental and vision care, allowing you to choose a plan that matches your healthcare needs more comprehensively.

These plans also often include Prescription Drug Plans (Part D), making them an all-in-one alternative that can simplify healthcare management for Medicare beneficiaries aged 60 to 85. It’s an opportunity to look beyond traditional plans for enhanced healthcare services that address a broader range of health concerns.

When enrolling in a Medicare Advantage plan, it’s crucial to note that these plans frequently carry specific service networks. It means you might be required to see doctors within the plan’s network to lower copayments and coinsurance costs. Though these plans come with their standards and cost structures, they must provide at least the same benefits as Original Medicare. However, additional benefits and premium variations may apply based on the chosen health plan.

The decision to opt for a Medicare Advantage plan should be informed by understanding the potential cost dynamics involving premiums, deductibles, copayments, and coinsurance. Each term affects what you pay out of pocket when accessing necessary healthcare services. It’s essential to evaluate how these plans differ from each other by contemplating location-specific offerings and individual healthcare needs.

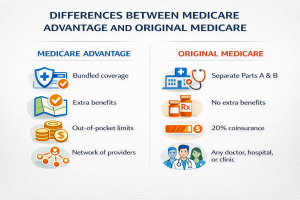

How Medicare Advantage Differs from Original Medicare

While Medicare Advantage plans provide a comprehensive solution by combining Medicare Part A and Part B, and often Part D, they differ significantly from Original Medicare in several ways. The primary difference lies in the flexibility and services.

Original Medicare allows beneficiaries to utilize any doctor or hospital participating in Medicare, providing broad access but often at the cost of higher coinsurance and copayments. Conversely, Medicare Advantage plans often have network restrictions, so beneficiaries may have to choose healthcare providers within an established network to manage costs effectively.

Financial aspects also set these plans apart. Medicare Advantage plans offer more predictable out-of-pocket costs with annual out-of-pocket maximums, providing financial protection against unexpected costs.

Most Medicare Advantage plans require copayments for doctor visits and coinsurance for other healthcare services, offering clarity that isn’t always present with Original Medicare. The tailored approach of these plans offers beneficiaries an option to select the best-suited plan according to their healthcare needs and financial capabilities.

It’s also worth mentioning that many Medicare Advantage plans include extra benefits, which can encompass dental, vision, and wellness programs not covered by Original Medicare. These added benefits make these plans an attractive option for those seeking beyond the standard Medicare coverage.

However, it is crucial to scrutinize each plan’s terms, as the additional benefits can vary significantly among the different insurance plans available. Making informed decisions can ensure that you’re getting comprehensive coverage suitable for your healthcare journey.

Exploring Copayment and Coinsurance

Navigating UPMC Medicare plans involves understanding the critical concepts of copayment and coinsurance, which are essential to managing your healthcare costs. Copayments refer to the fixed dollar amount you must pay for a specific service, while coinsurance is a percentage of medical costs you share with your insurance plan.

Both play significant roles in determining your out-of-pocket expenses. By grasping these concepts, you can better structure your Medicare Advantage plan to suit your healthcare needs while keeping medical costs manageable.

What is Copayment and How Does It Work?

A copayment, often referred to simply as a copay, is a fixed dollar amount you must pay when you receive a healthcare service. It’s a straightforward way to manage some of the costs associated with healthcare services under Medicare Advantage plans.

For example, when you visit the doctor or fill a prescription, you’ll likely encounter a copayment, which helps share the costs between you and your insurance provider. This fixed rate benefits you by reducing surprise medical costs, providing predictability, and helping with budgeting for recurring medical appointments and needs.

Copayments are especially common for routine doctor visits, specialist consultations, and prescription medications. They ensure that beneficiaries like you remain actively involved in managing healthcare expenses while protecting the insurance provider from absorbing all medical costs. The amount may vary by service type and health plan; some services may have higher copayments due to their complexity or the healthcare provider’s network status.

When enrolled in UPMC Medicare Advantage plans, your copayment amount becomes a crucial part of your budget, reflecting the insurance plan’s emphasis on offering transparent and predictable healthcare service costs. It forms the cornerstone of your out-of-pocket expenses, which makes assessing and comparing copayment amounts across different plans an important task during Medicare’s Annual Election Period.

For individuals researching the best plan options, understanding how these amounts can differ based on the service provided and the provider’s network can guide a more informed choice.

Recognizing the role of copayments in managing costs means not just looking at the dollar figures attached to each medical interaction but understanding how the broader structure of the plan works to balance affordability with access to necessary healthcare services.

This liberates beneficiaries to leverage the healthcare network effectively while keeping total medical expenses in check under the terms of their Medicare Advantage plan.

Find & Compare Plans Online

The Role of Coinsurance in Medicare Plans

Coinsurance is another key component in the landscape of Medicare Advantage plans, working alongside copayments to manage healthcare costs effectively. Unlike copayments, coinsurance is calculated as a percentage of the total medical costs, which means the amount you pay can vary depending on the service rendered and the total bill. This cost-sharing mechanism is essential in managing expenses for more significant and complex medical care and services.

For instance, after meeting a deductible, a set amount you pay out of pocket before your insurance starts to cover expenses, the insurance plan might cover 80% of a medical bill, leaving you with a coinsurance percentage of 20%. This approach ensures that both you and the insurer share the responsibility for healthcare costs. Coinsurance is particularly relevant for hospital stays, outpatient surgeries, and specialist consultations, where medical costs can fluctuate based on the services provided.

Understanding how coinsurance functions within UPMC Medicare plans can help you anticipate and manage potential expenses more effectively. Knowing your coinsurance amount allows you to plan for medical expenses, particularly for procedures or services outside routine care, where costs can quickly escalate. It’s a crucial element for those researching Medicare Advantage, especially when comparing plans to find one that aligns with their healthcare needs and financial situation.

Furthermore, coinsurance encourages a thoughtful engagement with healthcare services, where beneficiaries are incentivized to seek necessary care while being mindful of costs. This system promotes wiser healthcare decisions, ensuring that you’re using resources efficiently without sacrificing essential care.

With the insights gained from understanding the differences and interactions between copayments and coinsurance, individuals can make more strategic choices about their Medicare Advantage plan, resulting in better-managed healthcare budgets and improved peace of mind when accessing broad-ranging medical services.

Alongside coinsurance considerations, it’s essential to factor in the following elements to make informed healthcare choices:

- Verify which preventive services are fully covered without coinsurance obligations.

- Check annual out-of-pocket maximums to cap potential expenses efficiently.

- Assess any pre-approval requirements for specific treatments to avoid unexpected costs.

- Consider the impact of medication tiers on your total pharmacy expenses.

- Stay informed about any changes in network providers that may affect coverage.

- Understand the role of supplemental insurance in offsetting coinsurance payments.

- Look into wellness programs that may reduce overall healthcare spending.

These aspects, combined with coinsurance insights, will empower you to navigate your healthcare options with confidence and clarity.

Understanding Costs: Copayment vs. Coinsurance

Grasping the nuances of copayment and coinsurance is vital for managing your healthcare expenses under UPMC Medicare Advantage plans. Copayments involve a fixed amount for specific services, providing predictability in medical expenses. In contrast, coinsurance requires you to share a percentage of the total cost of healthcare services, influencing the overall financial responsibility.

This section delves into the intricacies of the coinsurance percentage and its calculation, offering clarity on how each aspect affects your overall costs and informs your decision-making as a Medicare beneficiary.

Analyzing the Coinsurance Percentage and Its Impact

Understanding the coinsurance percentage involves recognizing how a percentage-based system impacts medical expenses within your insurance plan. Unlike fixed copayments, the coinsurance approach requires a calculated share of costs, typically after meeting certain plan deductibles. This percentage can significantly influence your total healthcare expenses, particularly if the costs incurred are substantial.

For example, if your insurance plan dictates a 20% coinsurance percentage after the deductible, and you face a $1,000 bill for healthcare services, you’ll be responsible for $200 of that cost while your insurance covers the remaining $800. This mechanism ensures both parties contribute to the medical expenses, promoting shared responsibility.

The variability of coinsurance amounts can introduce unpredictability into your healthcare spending, necessitating careful planning and understanding. It’s crucial, therefore, to be familiar with your specific coinsurance percentage when evaluating different health plans, particularly those under UPMC Medicare Advantage.

Each plan might assign different coinsurance rates to various services like outpatient visits, hospital stays, or specialized treatments. This awareness helps you estimate potential expenses more accurately and prepare for higher costs associated with complex care. Anticipating these expenses can prevent financial strain and aid in crafting a comprehensive healthcare budget.

The payment structure influences healthcare decisions by encouraging beneficiaries to weigh the necessity and urgency of medical interventions against their potential costs. When examining a coinsurance percentage, consider its impact on accessing healthcare services and how it fits your overall medical needs and financial capabilities.

The balance between affordability and healthcare service access needs careful consideration. Such insights aid individuals aged 60 to 85, evaluating their insurance options, to select plans that align with their anticipated medical expenses and desired coverage levels, promoting informed plan choices.

Effective coinsurance management fosters a balanced healthcare approach, ensuring that medical costs for significant procedures remain manageable without compromising service quality or accessibility.

Comprehending this cost-sharing model enhances a beneficiary’s ability to make knowledgeable decisions about their insurance plan, optimizing both healthcare and financial outcomes. Investigating options with lower coinsurance percentages could be beneficial for those expecting high healthcare needs, offering greater financial predictability and protection.

How to Calculate the Coinsurance Amount

Determining the coinsurance amount involves more than simply understanding what percentage you or your insurance plan will cover. Proper calculations can ensure you are prepared for potential out-of-pocket expenses when utilizing healthcare services.

To begin, you’ll first need to know your total medical costs for a treatment or procedure, as well as whether you’ve met the annual deductible of your insurance plan. After meeting the deductible, coinsurance becomes the primary cost-sharing component.

Let’s say your deductible has been met. For a medical procedure costing $1,500 covered under your health plan with a 20% coinsurance rate, you calculate your responsibility by multiplying the total medical cost by your coinsurance percentage.

In this case, 20% of $1,500 results in a $300 out-of-pocket cost for you, while your insurance covers the remaining $1,200. This calculation helps you gauge the expenses linked to specific treatments, ensuring you can effectively budget for healthcare services.

Being proactive in calculating coinsurance amounts can enhance your confidence when accessing healthcare services under UPMC Medicare plans. This anticipation mitigates financial stress and enables strategic healthcare choices.

Moreover, understanding your coinsurance obligations can be constructive when planning for elective surgeries or treatments, where costs can be foreseen and accommodated within your financial planning. A detailed review of how these figures align with your maximum out-of-pocket limits within your Medicare Advantage health plan is also crucial to managing overall expenses and preventing financial surprises.

Finally, ensuring a comprehensive understanding of coinsurance allows individuals to maximize the benefits and coverage offered by their Medicare Advantage plan. By planning and preparing for potential expenses, you can use your plan’s features to your advantage, facilitating necessary care availability without incurring overwhelming costs.

Such financial awareness empowers beneficiaries to make informed decisions that reflect both their immediate healthcare needs and long-term financial health. Apt calculations and planning can turn insurance concerns into manageable aspects of your health coverage strategy, promoting confidence in navigating Medicare’s complex landscape.

| Aspect | Description | Impact on Costs | Example |

|---|---|---|---|

| Copayment | Fixed amount per service | Predictable expenses | $20 per doctor visit |

| Coinsurance Percentage | Shared percentage after deductible | Variable expenses | 20% of $1,500 = $300 |

This table underscores the distinctions and financial implications of choosing between copayment and coinsurance. It provides clarity for Medicare beneficiaries, allowing them to more effectively plan their healthcare expenses by understanding which method may lead to more predictable versus variable costs.

Comparing Coverage: UPMC Medicare Advantage Plans

Evaluating UPMC Medicare Advantage plans involves understanding their unique benefits and limitations compared to Original Medicare. These insurance plans aim to enhance healthcare services by integrating additional coverage options like dental and vision care, often including prescription drug plans.

However, examining the full scope of medical costs, copayments, coinsurance, and service limitations is essential to making informed choices. These factors significantly impact how effectively the plan meets an individual’s medical needs and financial situation.

Benefits and Limitations of UPMC Medicare Advantage

UPMC Medicare Advantage plans offer enhanced benefits, setting them apart from Original Medicare, making them a compelling choice for many beneficiaries. Primarily, these plans bundle Medicare Part A (hospital insurance) and Part B (medical insurance) into a single comprehensive health plan, sometimes including Part D for prescription drugs.

This integrated approach simplifies healthcare management, appealing to individuals seeking streamlined access to various healthcare services. Additionally, many UPMC plans cover additional benefits like dental, vision, and hearing, which Original Medicare typically does not offer, thus providing a more rounded healthcare package.

Aside from these added benefits, another significant advantage lies in the predictability of medical costs through established copayments and the inclusion of an annual out-of-pocket maximum. This feature offers beneficiaries financial protection, potentially limiting the overall medical costs they must manage each year.

When evaluating a Medicare Advantage plan, it’s vital to compare how these elements match personal health needs, as out-of-pocket costs can vary dramatically based on the specific services required and the chosen health plan’s structure.

Despite their advantages, UPMC Medicare Advantage plans are not without limitations. One such limitation concerns plan networks; many plans require beneficiaries to use a specified network of doctors, hospitals, and other healthcare providers.

This requirement potentially restricts the choice of healthcare providers and can impact accessibility, especially for those who prefer non-network providers. Moreover, although the plans are comprehensive, they might involve additional premiums compared to Original Medicare, varying based on factors like location and selected plan options.

Before choosing a UPMC Medicare Advantage plan, it is also important to understand the role of medical costs, such as copayments and coinsurance. These costs, alongside deductibles, contribute to the total out-of-pocket expenses, influencing the overall affordability of healthcare services.

Evaluating these costs in conjunction with potential healthcare needs, like routine visits or medical procedures, can guide beneficiaries toward plans that better balance coverage benefits with financial feasibility.

Careful consideration of the benefits and limitations of UPMC Medicare Advantage plans can aid Medicare beneficiaries in selecting an insurance plan that aligns well with their medical and financial priorities. For prospective enrollees, using resources like the free Medicare plans finder tool on MedicarePartCPlans.org can be invaluable.

This tool assists users in comparing health plans, fostering an informed decision-making process. By thoroughly comparing aspects of coverage, costs, and benefits, individuals can optimize their healthcare strategy efficiently under these plans.

Understanding the differences between copayment and coinsurance with UPMC Medicare plans is crucial for budgeting and making informed healthcare decisions. By familiarizing yourself with these cost-sharing methods, you can better predict your potential out-of-pocket expenses and plan accordingly. Be sure to evaluate how each plan’s structure aligns with your healthcare needs and financial situation.

For tailored guidance on selecting a suitable plan that meets your individual requirements, consider utilizing tools and resources designed to compare Medicare Advantage options. Stay informed and proactive in managing your healthcare costs to ensure you have access to necessary services when needed.

Compare plans and enroll online

Frequently Asked Questions

What are Medicare Advantage plans and how do they work?

Medicare Advantage plans, also known as Medicare Part C, provide an alternative way to receive your Medicare benefits through private insurance companies approved by Medicare. These plans must cover all services that Original Medicare covers and often include added benefits like dental, vision, and prescription drug coverage. They integrate Medicare Part A and Part B into a single plan, offering comprehensive healthcare coverage.

What is the difference between copayment and coinsurance in Medicare plans?

Copayment is a fixed dollar amount you pay for a specific service, offering predictability for budgeting purposes. Coinsurance is a shared cost, calculated as a percentage of the total medical costs after any deductible has been met. Both are critical components that influence your out-of-pocket healthcare expenses.

Example: If your coinsurance is 20% and you have a $1,000 medical bill, you would pay $200.

What additional benefits do UPMC Medicare Advantage plans offer?

UPMC Medicare Advantage plans offer additional benefits not typically covered by Original Medicare, such as dental, vision, and sometimes hearing services. Many plans also include Prescription Drug Plans (Part D), providing a more comprehensive healthcare solution.

What should I consider when choosing a Medicare Advantage plan?

When choosing a Medicare Advantage plan, consider factors such as premiums, deductibles, copayments, coinsurance, and your healthcare needs. It’s essential to evaluate whether the plan’s network suits your current healthcare providers and understand the limits of additional benefits. Comparing plans can help match your healthcare needs to the coverage provided.

How do UPMC Medicare Advantage plans handle healthcare networks?

UPMC Medicare Advantage plans often require beneficiaries to use a specific network of doctors, hospitals, and healthcare providers to manage costs effectively. This means that seeing providers within the network can help lower copayments and coinsurance costs, although it may limit provider choices compared to Original Medicare.

Have Questions?

Speak with a licensed insurance agent

1-877-436-2343

TTY users 711

Mon-Fri: 8am-9pm ET

Find & Compare Plans Online

ZRN Health & Financial Services, LLC, a Texas limited liability company